Shutterstock

WASHINGTON -- The average 30-year U.S. mortgage rate this week remained at a 52-week low of 4.10 percent for the third straight week.

Mortgage company Freddie Mac also said Thursday the average for a 15-year mortgage, a popular choice for people who are refinancing, slipped to 3.24 percent from 3.25 percent.

At its 52-week low of 4.10 percent, the rate on a 30-year mortgage is down from 4.53 percent at the start of the year. Rates have fallen even though the Federal Reserve has been trimming its monthly bond purchases, which are intended to keep long-term borrowing rates low. The purchases are set to end in October.

The low rates appear to have boosted U.S. home sales. Also, moderating increases in home prices such as occurred in July should help support sales by making homes more affordable. Real-estate data provider CoreLogic (CLGX) reported Tuesday that home prices rose in July but at a slower rate compared with earlier this year.

Greater affordability has helped the housing market recover over the spring and summer after sales and construction fell earlier this year. Sales of existing homes rose for a fourth straight month in July to their strongest pace in nine months. And a measure of signed contracts also increased in July, suggesting that final sales will rise further in coming months.

To calculate average mortgage rates, Freddie Mac surveys lenders across the country between Monday and Wednesday each week. The average doesn't include extra fees, known as points, which most borrowers must pay to get the lowest rates. One point equals 1 percent of the loan amount.

The average fee for a 30-year mortgage was 0.5 point, unchanged from last week. The fee for a 15-year mortgage fell to 0.5 point from 0.6 point.

The average rate on a five-year adjustable-rate mortgage was stable at 2.97 percent. The fee stayed at 0.5 point.

For a one-year ARM, the average rate edged up to 2.40 percent from 2.39 percent. The fee dipped to 0.4 point from 0.5 point.

Alamy

It may sound corny, but I truly believe almost anyone who lives in the United States can become a millionaire. As men and women living in this county, we are afforded opportunities to work hard, educate ourselves and build something from nothing.

I did all the above and became a millionaire before I turned 40. Here are the rules I followed:

1. Invest Every Windfall

When you receive an unexpected windfall such as an inheritance, cash gift or bonus, don't spend it. Invest it. If you weren't expecting the money, you're not depriving yourself of anything by not spending it.

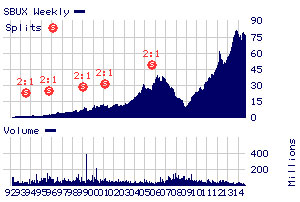

When I was 24, I received a $1,600 inheritance from my grandmother. Although I thought about buying clothes and shoes, I resisted the urge to adorn my body with depreciating assets and shopped for something far more valuable: stock in a publicly traded company. I remember the day I made my first-ever stock purchase. It was Jan. 27, 1993, and I bought 40 shares of Starbucks (SBUX) at $39¾ per share. Looking back, it was risky to put all my eggs in one basket, especially with a company that had only recently gone public and had no trading history. But as you can imagine, I got lucky.

Starbucks.com

Twenty-one years and five stock splits later, those 40 shares that cost me $1,600 would now be worth almost $100,000. I sold the shares long ago because as I matured as an investor, I decided to take modest gains by occasionally selling stocks and using the proceeds to diversify my investments across of wide range of companies.

2. Live Below Your Means

You've heard that advice a million times, haven't you? You keep hearing it because it really works. You can't build wealth if you spend more than you save. In my early 20s, I lived in a small, roach-infested, studio apartment in Washington, D.C. Until I was 27, my salary never exceeded $30,000. I was paying down student loans and generally didn't have a pot to piss in. But I made do.

I figured out early on the difference between needs and wants. The one exception was an expensive gym membership. Technically it was a "want," but for me it was a "need" because had I not had a venue to work off my stress, I would have gone postal.

Do I still live in a studio apartment? No. I'm married and live with my husband and stepdaughter in a three-bedroom townhouse. But I'm still living below my means.

3. Continually Invest Small Amounts of Money

When you live below your means by not upgrading your lifestyle every time you get a raise or promotion, you have more and more money to invest. The secret to not getting whipsawed by the stock market's volatility is to invest small amounts of money at regular intervals. You do this by default when you contribute to your employer's 401(k) or 403(b) plan.

Many people have remarked to me that their 401(k) took a beating during the 2008 stock market crash but recovered fairly quickly. That's because they kept putting in the same amount every paycheck and were able to buy shares of mutual funds on sale. This approach, called dollar-cost averaging, means you'll buy more shares when prices are low and fewer shares when prices are high.

4. Contribute to Retirement Accounts

If your employer offers a retirement plan, participate in it, especially if there is a match. The match is free money, which is essentially a 100 percent return on your investment for just showing up. There are many reasons why you might choose a Roth IRA over a traditional IRA or an IRA over a 401(k). In the grand scheme of things, they're all good.

When you sock away money in a tax-deferred account, you don't have to pay Uncle Sam and his offspring, the states, every year. Your money gets to compound like a snowball for many years until you take it out for retirement. With a Roth IRA, you don't pay any taxes when you take out the money at retirement.

A guy once commented on my Facebook page that I "was not really a millionaire" because more than a third of my wealth was tied up in retirement accounts and I couldn't access it. It's fair to say that most accountants, financial advisers and DailyFinance readers would disagree with that statement, as I surely do.

5. Pay Attention to Your Investments

We've all heard the rule, "buy and hold." I don't agree with that, because it often turns into "buy and ignore." As a financial adviser, I provide complimentary portfolio reviews to prospective clients. I would run out of fingers and toes if I tried to count how many people come to me with account statements showing stocks that once traded at $60 or $70 a share and now trade at $10 or $5 or don't even trade at all.

I'm agnostic on the question of whether you should hire a financial adviser/money manager or manage your money yourself. But if you choose the latter, you need to spend the time to educate yourself (or read my book) and review your portfolio on a regular basis. When I started investing, there was barely an Internet. I spent less time on my hair and makeup in the morning and more time reading the Wall Street Journal. With the plethora of free online resources available to you today, educating yourself is easier and cheaper than ever.

The information contained herein is strictly for educational and illustrative purposes, providing commentary, analysis, opinions, and recommendations and should not be considered investment advice for any specific subscriber or portfolio or an offer to sell or a solicitation to buy any security.

US Coast Guard via APBy Sudip Kar-Gupta and Karolin Schaps

HOUSTON -- BP was "grossly negligent" for its role in the 2010 spill in the Gulf of Mexico, a U.S. district judge said Thursday in a ruling that could add billions of dollars in fines to the more than $42 billion in charges taken so far for the worst offshore disaster in U.S. history.

Shares of BP (BP) traded in the United States fell 5 percent, or $2.40, to $45.31, eroding about $8.8 billion of its market value.

The Court concludes that the discharge of oil 'was the result of gross negligence or willful misconduct' by BP.

"The Court concludes that the discharge of oil 'was the result of gross negligence or willful misconduct' by BP, said the ruling from U.S. District Judge Carl Barbier in New Orleans.

BP said it would appeal the ruling.

The company was already forced to shrink by selling assets to pay for the cleanup of the disaster aboard the Deepwater Horizon drilling rig that killed 11 workers and spewed millions of barrels of oil for 87 days after the blast.

"Obviously the market's not taken it well and it was a little bit unexpected but you would expect BP to appeal the level of the fines, the decision made," said TJM Partners head of trading Manoj Ladwa said in London. "It is a short-term concern; longer term BP are cash generative and I'm sure they'll have the funds to pay for this."

Barbier has yet to assign damages from the spill under the federal Clean Water Act. Previous calculations by Reuters have shown fines could run to $17.6 billion in the costliest scenario.

A gross negligence verdict carries a potential fine of $4,300 per barrel fine, with BP having said some 3.26 million barrels leaked from the well and the U.S government having said 4.9 million barrels spilled.

Barbier apportioned 67 percent of the fault to BP, 30 percent to Transocean, which owned the drillship, and 3 percent to Halliburton (HAL), which did cement work on the Macondo well that blew out. Both of those companies have sought to limit their liability from the spill.

At least 20 styles of Disney (DIS) and Marvel branded kids' sunglasses were recalled because they were made with lead paint, in violation of federal law, the U.S. Consumer Product Safety Commission said Thursday. In addition, some sunglasses sold under the Sears (SHLD) and Kmart brand are being recalled.

Among the styles being recalled are those with Disney's Doc McStuffins, characters from the "Cars" movies, Jake and the Neverland Pirates and the Mickey Mouse Club. Marvel's Spider-Man sunglasses were also recalled.

Consumers are asked to take the recalled sunglasses away from children and contact the distributor to either get a refund or a free replacement sent to you.

200,000 Pairs Sold

More than 200,000 of the sunglasses were sold at CVS (CVS), Walgreens (WAG), Rite-Aid (RAD), Kmart, Bon Ton (BONT) and other stores between December 2013 and March 2014. They were priced at between $7 and $13.

The sunglasses were imported from China by the Rhode Island company FGX International. You can contact FGX at (877) 277-0104 weekdays between 8:30 a.m. and 4:30 p.m. Eastern.

Federal standards regarding lead in paints for products intended for children 12 and under have been tightened in recent years to allow virtually no lead at all -- only 0.01 percent, or 100 parts per million. Lead paint can be dangerous, particularly to young children who tend to put things in their mouths. Ingested lead has been connected to a variety of health problems in children, including neurological issues.

The funding status and levels of U.S. pensions is heading the wrong way. Despite a rising stock market, a report from the BNY Mellon Investment Strategy and Solutions Group is signaling that the funded Status of U.S. corporate pensions fell to 90.1%. On the flip-side, public pension plans, foundations and endowments gained in August. The biggest issue at hand still seems to be incredibly low interest rates. These keep pension funds from being able to meet certain income targets.

Falling interest rates led to higher liabilities and a lower funded status for the typical U.S. corporate pension plan in August. At the same time, rising asset values benefited public plans, foundations and endowments.

The typical U.S. corporate pension plan fell to 90.1% in August, and liabilities rose 3.3%, outpacing the 2.6% return for assets. This funded status is down 5.1% from the December 2013 high of 95.2%. The higher liabilities for corporate plans was shown to have resulted from the AA corporate discount rate falling to 4.11% over the month.

Public defined benefit plans in August exceeded their target by 1.3% as assets increased by 1.9%. The public plans also exceeded their target by 7.6% from the past year.

For endowments and foundations, the real return in August was 1.1%, as assets returned 1.8%. Private equity and real estate investment trusts returned 2.5% over the month. Foundations and endowments are ahead of the inflation plus spending target by 6.3% from the previous year.

Andrew D. Wozniak, head of fiduciary solutions at ISSG, said,

"Investors appeared to be torn between concerns about increased geopolitical tensions and optimism about the U.S. economy. Geopolitical concerns resulted in more interest in longer term corporate credit and government bonds, sending interest rates lower. Optimism about the economy helped to push equities and other risk-based assets higher."

The threat of extremely low interest rates hurting pension funds is not a new development. It has hurt the insurance sector in many cases too. Still, many would have hoped that this zero-rate QE-fueled economy would have been freed up to get to a normalized interest rate environment. That hasn't happened yet and is not expected to take place until 2015.

Here is one bit of food for thought — What if higher interest rates down the road are only moderately higher than the zero-rate or extremely low rate environment we are in now?

Jim Parkin/Alamy

NEW YORK -- A slump in oil prices weighed on the stock market Thursday, pushing the Standard & Poor's 500 (^GPSC) index to its third straight loss.

Stocks had started the day higher after the European Central Bank surprised investors by announcing that it had cut its benchmark interest rate to a record low and planned to purchase asset-backed securities in an effort to stimulate the region's ailing economy. Investors were also cheered by some encouraging reports on the U.S. economy.

The gains didn't hold though and the market fell back during afternoon trading, as the falling price of oil pushed energy stocks lower. Oil closed the day down 1.1 percent at $94.45 a barrel, dropping after government data showed that U.S. supplies fell less than expected last week. Traders may also have been reluctant to place big bets ahead of Friday's closely watched government jobs report.

Stocks have made a sluggish start to September, historically the worst month for the market, after surging in August. The S&P 500 gained 3.8 percent last month, climbing to a record high as it logged its best performance since February.

"The market did respond to the ECB news this morning and certainly to the good economic news, but there are definite signs that this market is stretched a bit," said Peter Cardillo, chief market economist at Rockwell Global Capital.

The S&P 500 index fell three points, or 0.2 percent, to 1,997.65. The index closed below the 2,000 points for the first time since it breached that level Aug. 29. The Dow Jones industrial average (^DJI) fell eight points, or 0.1 percent to 17,069.58 points. The Nasdaq composite (^IXIC) dropped 10.28 points, or 0.2 percent, to 4,562.29.

Stocks had climbed in early trading, following a move higher by major indexes in Europe, after the ECB's surprise announcement. Some analysts had been expecting the central bank to say it was preparing a new stimulus program, but most did not expect an announcement as early as this week.

The ECB said it had trimmed its benchmark interest rate to 0.05 percent from a previous record low of 0.15 percent. In a news conference, ECB President Mario Draghi also said the bank would also start purchases of private sector financial assets in October. The program aims to make credit cheaper, helping investment and growth at a time when the economy of the 18-country eurozone has stalled.

As well as boosting stocks, the announcement caused the euro to slump against the dollar, pushing it to its lowest level against the U.S. currency in more than a year. Europe's single currency, which has been in retreat over the past few weeks on expectations that the ECB may pursue further stimulus measures, fell 1.5 percent to $1.29 per euro.

There was also encouraging news for investors on the U.S. economy on Thursday.

U.S. services firms expanded in August at the fastest pace on record. The Institute for Supply Management said Thursday that its services index rose to 59.6 last month from 58.7 in July. The August figure is the highest recorded since the measure was introduced in January 2008.

Hiring is also picking up and U.S. businesses added jobs at a healthy pace in August, according to a private survey, the fifth straight month of solid gains. On Friday, the government will issue the August jobs report. The forecast is that U.S. employers added 220,000 jobs and that the unemployment rate dipped to 6.1 percent from 6.2 percent.

The early gains for stocks then faded in the afternoon as the energy stocks sagged, declining 1.3 percent, as the price of oil dropped.

Among other stocks making big moves, PVH (PVH) was the biggest gainer in the S&P 500.

The company, which owns of the Calvin Klein and Tommy Hilfiger brands, surged $11.25, or 9.6 percent, to $128.30, after reporting earnings that exceeded the expectations of Wall Street analysts.

Government bond prices fell. The yield on the 10-year Treasury note, which moves inversely to its price, climbed to 2.45 percent, from 2.40 percent late Wednesday.

In metals trading, gold closed down $3.80, or 0.3 percent, at $1,266.50 an ounce. Silver slipped 5.1 cents, or 0.3 percent, to $19.14 an ounce. Copper prices rose, climbing to 2.4 cents, or 0.8 percent, to $3.15 per pound.

In addition to oil, other energy prices fell. Heating oil dropped 3 cents to $2.836 a gallon and natural gas declined 2.8 cents to $3.819 per 1,000 cubic feet.

What to Watch Friday:

The Labor Department releases employment data for August at 8:30 a.m. Eastern time.

Getty Images

According to a recent report from the U.S. Travel Association, 40 percent of American workers don't use all their vacation days. The fact that so many Americans feel uncomfortable taking the time off that they've earned is disturbing -- and it doesn't have to be this way.

I remember that when I was growing up, my mother, a high school math teacher in the South, got 15 paid days of vacation every school year. She always said, "I earned them. I'm going to take them." That philosophy stayed with me when I grew up and started my own career.

Unlike most of my colleagues who roll over vacation days from year to year until they're told they must use them -- my employer only lets you bank 60 -- I closely monitor my time, take a few vacations throughout the year, and start fresh each January with a zero balance. That makes me an anomaly.

Many employees fear that if they take time off, their jobs won't be there when they return. Some believe they're more likely to be picked for layoffs if they're not around all the time. Others think that they're indispensable -- the whole place will grind to a halt without them, so they can't take a break. Our workaholic culture and fear for their careers holds others back: In many workplaces, there's a stigma against those who take prolonged time away from the office.

Regardless of unofficial policies, office politics or stigmatization, you are entitled to the amount of annual vacation that your employer promised you in your contract, and they can't officially penalize you for taking it. It's yours in the same way that your paycheck is. You've earned your vacation days, and you can and should take all of them, without fear. Here's how.

Be Reachable While on Vacation

With technology and smartphones, we may be able to go on vacation and still conduct those parts of your job that can't be left untouched for a week or two. Your clients don't always have to know where you physically are.

"Being reachable and productive even during vacation has become a way of protecting our 'brand' as employees," says Jenni Luke, CEO of Step Up, a nonprofit that recruits professional women mentors to propel girls from under-resourced communities. "Because technology makes us capable of being in touch at all times, employees today feel like they do not have an excuse to not be available.

Have Someone Watching Your Back

Adriana Ruiz, a public relations consultant with Newlink in Miami, recommends having a "trust buddy" system -- someone who's always watching out for you. "Having at least one person you can rely on for keeping your work afloat during the time you are outside of the office [helps] releases a lot of the pressure that comes with leaving work," she says.

There's a reason the military uses the buddy system. When someone falls down, it's easier to cover and help them and the company up again. Just make sure that it is someone you trust, who isn't looking to move up into your job. This works best when you work in teams.

Train Your Replacement

No one is irreplaceable, no matter what we want to believe about our work productivity and ourselves. If you are actually irreplaceable to your organization, you're probably not delegating enough to your staff and colleagues.

Our employers will replace us all one day. It's inevitable. In fact, training our subordinates to replace us helps show that we are ready to advance up the corporate ladder as well.

How else would there be places for us to advance if our bosses were irreplaceable? We need them to train us to move up, and we need to do the same for the workers that report to us. Your vacation can be a great test to see how your staff and co-workers rise to the occasion.

Let Your Intentions Be Heard

Don't keep it a secret that you are going to take some personal time. Let your boss and subordinates know with as much lead-time as you can give them. That will give everyone involved the time to plan ahead, and smooth over any bumps that may be caused by your absence.

"We plan ahead so that if someone is out, someone from our team will cover for them and let our clients know when their day to day person is going to be out and for how long and make sure they know who is their contact at the agency" says Carol Bell, a partner at BrandLink Communications. "Organization is key to being able to take time earned and really be able to enjoy it."

Coordinate Your Time Off with Your Boss

This is obvious, but it's worth saying: Some times will be better than others for you to be gone. If you're worried about the work you'll be leaving behind, have an open and honest discussion with your supervisor to find a vacation time that works for you and your company.

"You know when things in your company or department is not so hectic and where your position might not be required for a short time," says Carol Gee, a former editor at Emory University Business School Atlanta. "I made sure that any outstanding or critical tasks or deadlines were completed and relayed that to my supervisor when putting in request for leave."

Get a Second Opinion

Richard Kline, a hiring manager at LegalAdvice.com, recommends bouncing your vacation ideas and backup plan off an impartial third party.

"The trick is to gain an objective perspective and escape the 'office group fantasy' that taking a vacation is selfish," he says. "Quite often, discussions with people outside the office will assist people in realizing that the fear of taking a vacation is an unhealthy mindset that is to be overcome."

Have you ever been reluctant to take the vacation days you'd earned? Why? Was their an unwritten rule or feeling that it would be held against you? How did you get through it and still take your days off? Or did you?

Hank Coleman is the publisher of the popular personal finance blog Money Q&A, where he answers readers' tough money questions about investing, retirement, and other money matters. Follow him on Twitter @MoneyQandA.

Tom Wang/Shutterstock

If you think achieving higher expected returns on your investments is difficult, you are mistaken. But an even bigger mistake is assuming more money will make you happier.

Bigger Returns Are Achievable

Earning higher expected returns can be simple. Here is the process in three steps:

Determine what you want your asset allocation to be -- how you want to balance your portfolio between stocks and bonds. One way to help identify the right asset allocation for you is by taking a free risk-capacity survey, such as this one from Vanguard.

Create a globally diversified portfolio of low-cost, low-management-fee index funds.

Rebalance your portfolio once or twice a year to keep your actual asset allocation in line with your target balance, or to adjust the allocation if your investment objectives or tolerance for risk have changed.

I don't want to oversimplify the case for evidence-based investing (also called passive or index-based investing). Maintaining a disciplined investing plan can often be difficult for self-directed investors. When the inevitable market corrections appear, it can be emotionally challenging to rebalance by purchasing stocks when they're declining in value, and selling bonds when their value is increasing.

To achieve higher expected returns, it's extremely important that you ignore most of the financial media. It feeds you a daily grist of "financial psychics" pretending to have the expertise to pick winning stocks, time the market, and select "hot" fund managers. Once you understand that the "success" of such forecasts is most likely attributable to luck (and cherry picking their data after the fact), and not to skill, you'll be well on your way to capturing the market returns that are yours for the taking.

More Money Doesn't Mean Greater Happiness

Over the years, I've dealt with thousands of investors who were intensely focused on improving their returns. Understandably, many were concerned about having enough money to retire with dignity, if at all. I have been struck, however, by the number of wealthy and successful people I've met with an insatiable desire to increase their net worth, even though they'd already achieved financial success by any objective measure.

These people share one common characteristic. They are fundamentally unhappy. They believe increasing their net worth will make them happier. When they find it doesn't, instead of looking for the root causes of their unhappiness, they double down on their efforts to accumulate more assets.

I confronted the issue of trying to attain a higher level of happiness in my own life. When I achieved financial security, I found it didn't actually increase my happiness. I still felt there was no real purpose in my work or my life. I was trapped in an endless grind, with no "happiness payoff."

Shiny Objects, Unhappy People

My happiness breakthrough came when I started writing the "Smartest" series of investing books. They've been read by hundreds of thousands of investors all over the world. One was even translated into Chinese. I started getting emails from readers telling me how my books changed their lives. Some told heart-wrenching stories about how they were victimized by their brokers and advisers. As a result, I found a purpose in my life that transcended my self-interest. The realization that I touched people's lives in a positive way has made me a much happier person, content with my life and very grateful for it.

I touched people's lives in a positive way, which has made me a much happier person.

You wouldn't think it would be necessary to extol the virtues of being happy. There is ample evidence that happiness is positively linked to living a longer life, and even to having an improved immune system. Much has been written about how to achieve happiness. But a good start is by focusing on positive relations with others, and on demonstrating genuine empathy. You can try using these 25 science-backed ways to be happy.

Achieving financial security is a very worthy goal. Doing so at the expense of your own happiness is a flawed plan. Fortunately, you can have both.

Dan Solinis the director of investor advocacy for the BAM Allianceand a wealth adviser with Buckingham. He is a New York Times best-selling author of the Smartest series of books. His latest book is "The Smartest Sales Book You'll Ever Read."

Brian Jackson/AlamyOnline investment management tools can motivate you to control spending and save more.By Robert Berger

Saving for retirement certainly isn't easy. A recent study by the Transamerica Center for Retirement Studies found that only 18 percent of those surveyed expect to be better off in retirement. While no tool can fully automate retirement planning, there are tools that can offer a lot of help. These six tools can help you save, plan and prepare for your golden years:

1. Personal Capital. This free tool is the Cadillac of investment tracking tools. Not only does it track investment performance, but it also shows you your asset allocation across all investment accounts, including taxable and tax-advantaged accounts. For those with a 401(k), Personal Capital also shows you how the costs of the retirement account affect your ability to retire. The graphs and charts make understanding all of your investments very easy.

2. Money Ratios. Popularized by a book of the same name by Charles Farrell, Money Ratios offers an easy way to determine if you are saving enough for retirement. The simple ratios can show you if your saving rate is sufficient, and if your current nest egg, given your age and income, has you on a secure path to retirement. In addition, the book provides ratios to help you evaluate your debt, mortgage and other important financial planning issues.

3. You Need a Budget. At the heart of both saving for retirement and making your nest egg last in retirement is money management. YNAB is an excellent budgeting tool. Having used it for years, it's helped me actually stick to a budget. In addition to the tool, YNAB offers an excellent series of videos, articles and an active user forum to help you use its tools and better manage your money.

4. Social Security calculator. The Social Security Administration offers a free calculator that helps you estimate the Social Security benefits you will receive in retirement. In addition, you can get a statement from SSA with a breakdown of your contributions and expected future benefit. The SSA also offers life expectancy and retirement age calculators.

5. Retirement calculators. There are a lot of free retirement calculators available online. Some are very simple, while others require more data and undertake a more complex evaluation. One of the most thorough options is the Flexible Retirement Planner. But be prepared to spend some time with the calculator. For example, you can create "what if" scenarios to evaluate how certain life events may affect your retirement readiness. You can also perform a sensitivity analysis to determine which factors will have the greatest impact on your retirement.

6. A credit card. Yes, even the credit card industry has waded into the retirement planning industry. One of my favorite cash back credit cards is the Fidelity Investment Rewards American Express. The card pays 2 percent cash back on all purchases and deposits the rewards in your Fidelity account. It's one of the most rewarding credit cards available today. Now if only other investment firms would join the party.

Rob Berger is an attorney and founder of the popular personal finance and investing blog, doughroller.net. He is also the editor of the Dough Roller Weekly Newsletter, a free newsletter covering all aspects of personal finance and investing, and the Dough Roller Money Podcast.

Getty Images

Buying a home has been part of the traditional American dream for decades. However, it's a big financial commitment, and one that can haunt you for years if you jump in before you're ready.

The cost of you new home will extend far beyond your initial down payment. Don't forget to also consider the mortgage origination fees, closing costs, principal and interest, homeowner's insurance, and property taxes. Then there are utilities, renovations, home owner's association fees and the typical day-to-day maintenance costs that come with owning a home and replacing items as they age.

Understand Your Finances

Costs of home ownership aside, there's the question of whether you're in a strong position financially to make the purchase. Only after you can check off these items should you proceed:

You're on track with your financial goals. This means you've established and are consistently funding retirement accounts and that you have eliminated all consumer debt or at least have a strong handle on it.

You have a full emergency fund. You have three to six months of expenses stocked away.

Your credit score is good or excellent. A good credit score translates into a lower interest rate and thousands of dollars saved over the life of the loan.

You've run the monthly numbers. Your total living expenses with your new home should not equal more than about 25 percent of your current budget.

If you have these areas covered, the next step is to answer a few questions about your personal situation.

Do we know where we'd like to live for the next five years? If you're thinking of relocating or moving, you may want to wait until things are more settled to buy for the long-term. A turnaround sale could have you losing money right off the top.

Do we have job security? If your work is highly unstable, think about how you'd make the payment if you lost your income. If you don't have the funds to cover it or a plan in place, again -- you may want to wait until you're in a more stable situation.

Are we ready to maintain a home on a consistent basis? Plumbing issues, yard maintenance and more come with a house. Make sure you're ready to handle it yourself or shell out the funds to hire those to do it for you.

Do we have a down payment? How much do you need for a down payment on a home in your area and what does that translate into for monthly expense? Make sure you have the cash you need on hand.

You should have at least 20 percent of the home's purchase price saved for the down payment. Any less and you'll likely be paying private mortgage insurance, designed to protect the lender in case the borrower defaults.

Understand How to Save

If you've made it to the point of saving for a down payment, you know that 20 percent of a home's purchase price is a big number. Try one of these strategies for saving up a home down payment:

Establish a special savings fund. This is a big goal that deserves its own savings account. Look for a savings account online or at a local credit union that can offer you a decent interest rate.

Slash unnecessary expenses. Review your expenses and note what you're willing to cut out or reduce in order to save for this goal and reallocate the funds to your new account.

Swap it out. Swap expensive habits for cheaper alternatives, such as dining out to lunch instead of dinner, working out at home instead of at the gym, etc. Track new habits to determine extra funds on hand and transfer those savings to your home down payment fund.

Create a budget and make room for savings. If you don't already use one, establish a budget that includes your monthly down payment savings and stick to it each month.

Keep extra money. Whenever you receive extra cash, make it a rule to put 80 percent into your savings and spend 20 percent on yourself.

Grow your income. If you want to pick up the pace on saving, work overtime, negotiate a raise or establish your own side hustle to earn extra money in your spare time.

www.roominatetoy.com

Women earn more bachelor's degrees than men, but not in the hot fields known as STEM -- science, technology, engineering and mathematics -- according to a 2013 National Science Foundation study. There is no concrete evidence as to why women account for only 13 percent of engineers, but lingering social stigma around girls who show interest in math and science is widely considered one prominent cause of this disparity. Which is why one startup firm is focusing on that dispelling that mindset among the youngest demographic they can reach.

Roominate Steps In

Roominate, winner of 2013's Oppenheim Toy Portfolio Platinum and Parents' Choice Gold Award, was the brainchild of Alice Brooks and Bettina Chen, who earned master's degrees in engineering at Stanford. After talking about the glaring gender imbalance in their field and program, the two set out to create toys that would teach girls how much fun building something new can be, and plant the seeds in their minds that could later lead more of them to pursue engineering, reports The Wall Street Journal. Key words from the home page of Roominate -- build, wire, design and customize -- reflect the kinds of things engineers do.

Their plan to get girls to build structures, and gain hands-on skills and self-confidence, quickly resonated with supporters. A spring 2012 Kickstarter campaign saw Roominate triple its original goal to fund its line of pastel-colored assembly pieces. That was followed by funding from angel investors in 2013.

Roominate is already seeing its success in the form of completed project photos from their 'Young Inventors', such as Golden Gate Bridge re-creations and cotton candy machines. Five new Roominate products are slated to hit chains including RadioShack (RSH) and Walmart (WMT) this fall -- among them, more elaborate houses, submarines and rockets.

Getting Excited

Brooks said she "grew up playing in her dad's robotics lab. When she asked for a Barbie, he gave her a mini-saw. So she made her own doll." On Roominate's website, Chen said she made "hundreds of extravagant creations" from Lego pieces as a child. They want to inspire similar creativity in younger girls.

Roominate isn't the only toy that can give girls the confidence that they can have a STEM career when they grow up. Mattel's (MAT) Barbie, who's held other tech jobs before, has also been cast as a computer engineer.

Girls in need of more than a doll to inspire them should consider an array of do-it-yourself kits from companies like littleBits or GoldieBlox, an Oakland, California, firm that this year became the first small business to run a Super Bowl ad. Founder Debbie Sterling, another Stanford engineering grad, notes on the GoldieBlox site that the toys entertain and teach such basic engineering principles as wheels, axles, force, friction, gears, hinges and levers. "Future toys will explore pulleys, gears, levers, circuits and even coding," she said.

Cathleen Allison/APTesla Motors CEO Elon Musk, left, and Nevada Gov. Brian Sandoval at a press conference Thursday announcing the new site for the company's new $5 billion car battery plant.By SCOTT SONNER and JUSTIN PRITCHARD

CARSON CITY, Nev. -- Gov. Brian Sandoval announced Thursday that Nevada won a high-stakes battle with four other states for Tesla's coveted battery factory, but the win comes with a hefty price tag -- up to $1.3 billion in tax breaks and other incentives over 20 years that state lawmakers still must approve.

Sandoval revealed terms of the deal he negotiated with the electric car maker at a ceremony on the Capitol steps attended by Elon Musk, CEO of California-based Tesla Motors (TSLA). Musk confirmed the search was over for a home for his $5 billion lithium battery "gigafatory," which the company hopes will bring it closer to mass production of a more affordable electric car.

The Republican governor called it a "monumental announcement that will change Nevada forever" and asserted that it would create more than 22,000 jobs and pump $100 billion into the state's economy over the next 20 years -- claims that critics said were exaggerated. Sandoval didn't mention the total value of the incentive package in his remarks but nonetheless anticipated potential criticism for the size of the package.

"Even the most skeptical economist would conclude that this is a strong return [on investment] for us," he said about the deal that already has drawn outside criticism from both the political left and the right that the tax breaks are too generous. So far, it has not encountered significant opposition from state lawmakers who must approve the incentives.

Musk told the audience that Nevada didn't offer the biggest incentive package among the five states that tried to lure the factory, though he didn't specify which did among California, Texas, Arizona, New Mexico and Nevada.

The most important considerations were not incentives, he said, but rather a high confidence that the factory will be ready by 2017, followed by assurances that batteries can be produced cost efficiently.

"It's a real get-things-done state," Musk said in explaining how Nevada prevailed in what was a "relatively close" competition.

Musk, who arrived from London just before the ceremony, briefly bungled the pronunciation of "Nevada." But he recovered and twice received standing ovations from more than 200 dignitaries.

Later, Musk told reporters that Tesla would stop looking for another state as a backup. "Nevada is it," he said.

Special Session

The governor will call a special session of the Legislature as early as next week to seek approval of the incentives. Legislative leaders have reacted largely favorably at first blush.

House Speaker Marilyn Kirkpatrick, D-Las Vegas, said it represents "a significant opportunity to make a major stride to boost the economy" in a state that led the nation in unemployment during the depths of the Great Recession.

"I look forward to receiving the necessary information so the Legislature can meet and take necessary action to support this major industry coming to Nevada," she said in a joint statement with Sandoval and Musk that the governor's office issued Thursday.

Tesla's choice for the facility gets it closer to mass producing an electric car that costs around $35,000 and can go 200 miles on a single charge. That range is critical because it lets people take most daily trips without recharging, a major barrier to the widespread adoption of electric vehicles.

The factory would bring down the cost of batteries by producing them on a huge scale. The facility would be approximately 10 million square feet, equivalent to about 174 football fields, and be located at an industrial park about 15 miles east of Sparks, a Reno suburb founded as a railroad town more than a century ago.

The ultimate cost of the incentive package to Nevada taxpayers depends on how much economic activity the factory generates. On the low end, it could be worth $865 million, according to Steve Hill, executive director of Sandoval's Office of Economic Development.

Hill projected the factory would generate roughly $5 billion a year for 20 years for Nevada's economy and directly or indirectly create 22,000 new jobs over two decades. That includes an estimated 6,500 permanent jobs at the factory with hourly wages above $25 and a peak of 3,000 construction jobs leading up to the opening of the plant in 2017.

Large Subsidy

He also that even with the tax breaks, the project should generate approximately $1.9 billion in tax revenue for all levels of government -- state, local and school districts.

The largest subsidy for an auto-related plant was $1.3 billion that Chrysler received in 2010 to build an assembly plant in Michigan, according to the research group Good Jobs First, which tracks large incentive packages by states.

The group's executive director, Greg LeRoy, said Sandoval's projections of job creation and return on investment for the Tesla factory were implausibly rosy.

The governor said that every $1 Nevada invests in the effort will bring $80 back to the economy. LeRoy called that assertion "off the charts false." What he described as the proper calculation of tax breaks to tax revenues would put the return on investment at $2 or less for every $1 invested.

LeRoy also said the factory would create no more than about 10,000 permanent, non-construction jobs outside the factory, bringing the total to 19,500 -- not the 22,000 that Sandoval's administration claimed.

NEW YORK -- Americans' obsession with jeans is beginning to wear thin.

Jeans long have been a go-to staple in closets across the country. After all, not many pieces of clothing are so comfortable they can be worn daily, yet versatile enough to be dressed up or down.

But sales of the iconic blues fell 6 percent during the past year after decades of almost steady growth. Why? People more often are sporting yoga pants and leggings instead of traditional denim.

The shift is partly due to a lack of new designs since brightly colored skinny jeans were a hit a couple years back. It's also a reflection of changing views about what's appropriate attire for work, school and other places that used to call for more formalwear.

"Yoga pants have replaced jeans in my wardrobe," said Anita Ramaswamy, a Scottsdale, Arizona high-school senior who is buying more leggings and yoga pants than jeans. "You can make it as sexy as skinny jeans and it's more comfortable."

To be sure, the jeans business isn't dead: Customer Growth Partners, a retail consultancy, estimates denim accounts for 20 percent of annual sales at the nation's department stores.

But sales of jeans in the U.S. fell 6 percent to $16 billion during the year that ended in June, according to market research firm NPD Group, while sales of yoga pants and other "active wear" climbed 7 percent to $33.6 billion.

And Levi Strauss, which invented the first pair of blue jeans 141 years ago, is among jean makers that acknowledge their business has been hurt by what the fashion industry dubs the "athleisure" trend. That's led them to create new versions of classic denim that are more "stretchy" and mimic the comfort of sweatpants.

Birth of the Blues

It's one of the few times jeans haven't been at the forefront of what's "trending." Businessman Levi Strauss and tailor Jacob Davis invented jeans in 1873 after getting a patent to create cotton denim workpants with copper rivets in certain areas such as the pocket corner to make them stronger. By the 1920s, Levi's original 501 jeans had become top-selling men's workpants, according to Levi's corporate website.

Over the next couple of decades, the pants went mainstream. In 1934, Levi's took advantage of the rise in Western movies and launched its first jeans aimed at affluent women who wanted to wear them on dude ranches. Then teens boosted popularity of the pants, first among the greasy-hair-and-leather-jacket-set in the 1950s and then, the hippies in the 1960s.

But teens' biggest contribution to jeans' rise was the name itself: Until the 1950s, the pants were called overalls or waist overalls, but in the following decade, teens started referring to them as jeans. During that time, jeans took on a bad-boy image -- popularized by teen rebels such as James Dean and Marlon Brando -- which led many schools to ban kids from wearing them to class.

In 1960, Levi's began using the "jeans" name in ads and packaging. And over the next few decades, jeans became even more of a way for people to express themselves. In the 1960s to early 1970s, hip-huggers and bell bottoms became an anti-establishment statement. Then in the 1970s and early 1980s, jeans became a status symbol when designers such as Jordache rolled out more chic versions. More recently, names such as 7 For All Mankind made $200 jeans, helping to push sales up by 10 percent to $10 billion in 2000, NPD said.

Ironing It Out

Jeans have faced other rough patches. One came in the mid-1970s, when denim sales fell three to four percent, while corduroy pants surged in popularity, with sales rising 10 to 12 percent, according to NPD estimates.

NPD declined to offer more historical sales data because of changes it made in its methodology recently, but the group's chief industry analyst Marshal Cohen says jean sales fell about 3 percent again with the resurgence of khakis 12 years ago. That was the last decline until now.

Fashion watchers say the latest decline could be the longest. The "athleisure" trend is the biggest threat jeans have faced because it reflects a fundamental lifestyle change, said Amanda Hallay, assistant clinical professor of fashion merchandising at LIM College in Manhattan. "Everyone wants to look like they're running to the gym, even if they're not," she said.

As a result of jeans' waning popularity, retailers and designers are focusing more on activewear and less on denim. For instance, J.C. Penney (JCP) recently has doubled its selections in casual athletic looks and scaled back growth of its denim business.

And designers are pushing new versions of jeans. Both Levi's and VF Corp. (VFC), the maker of Wrangler and Lee jeans, are rolling out jeans that they say are stretchier. And many brands are making so-called jogger pants, a loose-fitting, sweatpant style that has elastic cuffs at the bottom of the leg.

"If casualization is what everyone is looking for, we can push the innovation," said James Curleigh, president of the Levi's brand.

It's too early to tell whether the new styles will help jeans regain popularity. Jennifer Romanello, for one, said she's not interested in them.

"If I want yoga pants, I will buy yoga pants," said the publishing executive from Rockville Centre, New York. "I just don't see jeans crossing the line to be yoga pants."

Apple (AAPL) is planning additional steps to keep hackers out of user accounts in the face of the recent celebrity photo scandal and will aggressively encourage users to take stricter security measures, CEO Tim cook told The Wall Street Journal in an interview.

Apple will alert users through email and push notifications when someone tries to change an account password, restore iCloud data to a new device, or when a device logs into an account for the first time, the report said.

Apple is moving quickly to restore confidence in its systems' security ahead of the crucial launch of its new iPhone next week.

Cook said Apple will broaden its use of the two-factor authentication security system to avoid future intrusions, the Journal reported.

The two-factor authentication requires a user to have two of three things to access an account, which may include a password, a separate four-digit one-time code, or a long access key given to the user when they signed up for the service.

The iPhone maker said it plans to more aggressively encourage people to turn on the two-factor authentication in the new version of iOS, the daily reported.

"The usability battle will always be there but could you ever imagine using your debit card at an ATM and not entering a pin? That's two factor, something you have [a card] & something you know [a pin], and we all get along just fine," WhiteHat Security's Matt Johansen told Reuters.

Apple said Tuesday the attacks that emerged over the Labor Day weekend on celebrities' iCloud accounts were individually targeted, and that none of the cases it investigated had resulted from a breach of its systems.

Some security experts have faulted Apple for failing to make its devices and software easier to secure through two-factor authentication, which requires a separate verification code after users log in initially.

Apple could also do more to advertise that option, they said. Most people don't bother with security measures because of the extra hassle, experts say, and the leading phone makers are partly to blame.

The iCloud service allows users to store photos and other content and access it from any Apple device. Security in the cloud has been a paramount concern in past years, but that hasn't stopped the rapid adoption of services that offer reams of storage and management of data and content off smartphones and computers.

WASHINGTON -- employers hired the fewest number of workers in eight months in August and more Americans gave up the hunt for jobs, providing a cautious Federal Reserve with more reasons to wait longer before raising interest rates.

Nonfarm payrolls increased 142,000 last month after expanding by 212,000 in July, the Labor Department said Friday. The jobless rate fell one-tenth of a percentage point to 6.1 percent, but that was partly because people dropped out of the labor force.

Data for June and July were revised to show 28,000 fewer jobs created than previously reported. In addition, manufacturing saw no job growth and retail payrolls declined for the first time since February.

The underlying message appears to be that the U.S. labor market recovery, which until this month appeared to have been firing on all cylinders, has hit a snag.

"The underlying message appears to be that the U.S. labor market recovery, which until this month appeared to have been firing on all cylinders, has hit a snag," said Millan Mulraine, deputy chief economist at TD Securities in New York.

The report did, however, suggest that some of the slack in the labor market was being taken up.

U.S. stocks opened down slightly, while price for U.S. Treasury debt rose and the dollar fell against a basket of currencies. Interest rate futures, which had been pointing to a likely rate hike in June of next year, rose to suggest less of a chance. However, they still showed dealers expect the Fed to bump up borrowing costs in July.

Economists had expected payrolls to increase by 225,000 in August. Many analysts said they were taking the report with a grain of salt given that it was at odds with other labor market indicators, such as first-time applications for unemployment benefits, which are hovering near their pre-recession levels.

In addition, manufacturing and service sector surveys showed strong employment growth in August and household perceptions of the labor market brightened significantly.

"The preponderance of evidence is that the economy is still gaining a lot of traction," said Russell T. Price, senior economist at Ameriprise Financial (AMP) in Troy, Michigan.

Number of Long-Term Unemployed Eases

Fed Chair Janet Yellen has expressed concern about sluggish wage growth, the still-elevated numbers of Americans working part-time even though they want full-time employment, and Americans still suffering from long spells of joblessness.

The U.S. central bank, which has held benchmark interest rates near zero since December 2008, has pointed to these metrics as evidence of "significant underutilization" of labor market resources that merits a stimulative monetary policy.

The labor force participation rate, or the share of working-age Americans who are employed or at least looking for a job, fell to 62.8 percent in August from 62.9 percent in July.

But other metrics on Yellen's so-called dashboard showed improvement.

A broad measure of joblessness that includes people who want to work but have given up searching and those working part-time because they can't find full-time employment fell to 12 percent, the lowest level since October 2009. The gap between that figure and the official unemployment rate narrowed, a further sign of tightening labor market conditions.

At the same time, the number of long-term unemployed Americans was the lowest since January 2009.

Average hourly earnings rose 6 cents in August, which marked an acceleration from July. Still, the year-on-year change held at 2.1 percent, which suggests little buildup of wage-related inflation pressure.

The Fed next meets on Sept. 16-17 to debate the course of monetary policy.

The private sector accounted for the bulk of the increase in payrolls in August, with the number of jobs increasing 134,000 after rising 213,000 in July. Government employment increased 8,000 as state governments hired teachers at the start of the new school year.

Manufacturing payrolls were the weakest in a year. The sector had added a hefty 28,000 jobs in July, which reflected a decision by automakers to keep assembly lines running in the summer. Auto payrolls fell 4,600, the first decline since March.

Construction employment advanced 20,000, rising for an eighth straight month. The length of the average workweek held steady at 34.5 hours for a sixth month in a row.

-With additional reporting by Herb Lash in New York.

Ben Torres/Bloomberg via Getty Images

CHESAPEAKE, Va. -- Family Dollar is rejecting Dollar General's latest acquisition offer, and Dollar Tree says it will now divest as many stores as needed to get antitrust clearance for its deal to buy Family Dollar.

Family Dollar rejected an earlier offer of nearly $9 billion from Dollar General, with the Goodlettsville, Tennessee, discounter then boosting its bid to $9.1 billion. Dollar General -- the nation's biggest dollar-store chain -- had also revised its proposal to increase the number of stores it would be willing to divest and to include a $500 million reverse break-up fee to Family Dollar if the deal hit antitrust roadblocks.

But Family Dollar said Friday that it still has antitrust concerns. Dollar General didn't immediately respond to an email seeking comment.

Family Dollar has been looking for a lifeline after running into some financial stress, shuttering stores and cutting prices. In June one big shareholder, Carl Icahn, urged the Matthews, North Carolina-based company to put itself up for sale.

A month later Family Dollar Stores (FDO) accepted an $8.5 billion deal with Chesapeake, Virginia-based Dollar Tree (DLTR). The transaction includes $59.60 in cash and the equivalent of $14.90 in shares of Dollar Tree for each share held. The companies valued the transaction at $74.50 a share at the time. Including debt and other costs, Family Dollar and Dollar Tree estimated the deal to be worth approximately $9.2 billion.

The two companies said Friday that they anticipate the transaction closing as early as the end of November.

Dollar Tree's willingness to shed more stores comes three days after Dollar General (DG) said it would divest up to 1,500 stores to get a deal done. Dollar General originally agreed to shed 700 stores.

Dollar Tree CEO Bob Sasser said in a statement that he believes the company would be required to divest few, if any, of its stores because its business model is significantly different from Family Dollar's.

"Our product assortment and pricing is not driven by local competition, and we have very limited store overlap," he said.

The businesses of Family Dollar and Dollar General are more similar than Dollar Tree's. The first two sell items at a variety of prices while at Dollar Tree, all items are a buck.

Aside from agreeing to potentially divest more stores, all other terms of Dollar Tree's deal with Family Dollar are unchanged.

Family Dollar and Dollar Tree said that they expect the Federal Trade Commission to put forth a second request for additional information on their proposed transaction on Monday. The companies said that they are confident they will receive regulatory approval for the transaction.

Family Dollar's stock fell $1.05 to $79.01 in morning trading, while shares of Dollar Tree rose 16 cents to $55.18. Dollar General's stock declined $1.39, or 2 percent, to $63.09.

Andy Dean Photography/Shutterstock

About 38 million Americans now rely on Social Security benefits after they retire, and with growing numbers of baby boomers adding their names to the rolls of Social Security recipients, that number is only going to increase in the years to come. But if you're younger than 60, there's something you need to know about your Social Security benefits -- especially if you were counting on retiring at a certain age.

Many people think of age 65 as the natural time to retire, with early retirees often aiming for age 62. Yet even though Social Security benefits are available to Americans as early as their 62nd birthday, coming changes to the official full retirement age will mean bigger reductions in benefits for early retirees and longer waits for those seeking the full amount of benefits they're entitled to get.

Pushing Retirement Back

For those born from 1943 to 1954, the officially sanctioned full retirement age -- when retirees can apply for Social Security and get the full calculated amount of their monthly benefits -- is 66. Wait beyond your full retirement age, and many Social Security recipients can get money added to their monthly checks. Begin taking benefits early, and you'll take a hit to the amount you receive.

But beginning for those born in 1955, who will be eligible to apply for benefits as early as 2017, the full retirement age will start going up. For today's 59-year-olds, the official full retirement age will be 66 and two months, and for every year after that, the age will go up by another two months until it hits 67 for those born in 1960 and later.

Raising the full retirement age acknowledges lengthening lifespans and reflects a greater willingness among American workers to work longer. But it also has a financial impact on Social Security recipients regardless of when they start collecting benefits.

Watching the Numbers Fall

A rising full retirement age hits workers by increasing the penalty they take for claiming early benefits. For those entitled to full benefits at age 67, claiming Social Security at age 62 incurs 60 months' worth of penalties -- rather than 48 months for current retirees with a full retirement age of 66.

Right now, those retiring at age 62 take a 25 percent haircut off the benefits they would receive if they waited until age 66. But once the retirement age goes up, the amount of the decrease will get bigger, with the Social Security Administration lopping off 30 percent from the monthly benefit for those currently younger than age 55.

The same thing happens for those who expect to wait beyond full retirement age to collect their Social Security benefits. Currently, if you wait until age 70, you get four years of what are known as delayed retirement credits, which boost your monthly benefit amount by 8 percent per year for a maximum of 32 percent. But when the full retirement age goes up to 67, the maximum available boost will be three years, or 24 percent.

Those expecting to receive spousal benefits also have to be aware of potential reductions in what they'll receive from Social Security. The current 30 percent reduction to spousal benefits at age 62 will become a maximum 35 percent cut once the full retirement age hits 67.

What Can You Do?

Unfortunately, there's little that Americans can do about the planned increase in the full retirement age for Social Security benefits. The legislation that enacted the increase became law back in 1983, when the retirement age was 65. Nothing happened under that legislation to change the retirement age until 2000, when it started its rise (now already completed) from 65 to 66.

Nevertheless, knowing that your benefits will be correspondingly lower than that of today's current retirees gives you some options to change your future strategy. By working longer, you'll avoid the benefits reductions that those with no choice but to claim Social Security at their first opportunity will have to accept in order to retire.

Steve Mawyer/AOL

The next time Disney (DIS) raises the bar when it comes to in-park entertainment, don't be surprised if an army of drones is holding up that bar. The family entertainment giant published some interesting patent applications late last month for concepts that could wow audiences, with unmanned aircraft vehicles doing a lot of the heavy lifting.

One patent covers drones that would be used to lift large aerial marionettes in the air. Several drones would be attached to the body and articulated appendages, running preprogrammed routes. Holy Pinocchio! (One illustration accompanying the patent shows Jack Skellington.)

Another patent would find a fleet of drones raising flexible mesh screens where projectors would be able to blast images and other effects onto the moving surfaces. Patent images show these large projector screens canvassing high above the park's signature castles, where Disney presently hosts its nighttime fireworks displays.

The third patent covers drones as floating pixels. They aren't carrying Disney characters or mesh screens this time. The unmanned aircraft vehicles would instead be equipped with multicolored lights and other effects that could be used to illuminate the sky, likely in sync to a symphonic score of Disney classic songs.

Up in the Air

Disney tested drones out two years ago with the opening of the New Fantasyland expansion at Disney World's Magic Kingdom in Florida. In the days leading up to the official opening of the most ambitious expansion in the park's history, Disney's blog teased about dragon sightings, culminating in an actual flying dragon that wowed travel journalists and bloggers who were invited to the after-hours grand opening.

Daytime guests never got to see the dragon in action. Despite the initial hype, the unmanned aircraft vehicle dolled up as an audio-animatronic dragon was limited in its watch over New Fantasyland. Was the dragon unreliable? Were there concerns that park guests would freak out if they saw the winged creature in action? Were there safety concerns that the dragon would falter or crash into something and come plunging into a sea of patrons?

The dragon didn't live long, but Disney filed the three patent applications just two months later. Sooner or later, Disney's going to raise the bar with drones enhancing its entertainment.

Drone Dreams

Disney isn't afraid to spend big money on technology that enhances the theme park experience. It spent a reported $1 billion last year to roll out MyMagic+ scanning technology that allows guests donning RFID bracelets to reserve ride times, enter the park and eventually receive tailored experiences.

When Disney adds a new ride, it may not be as thrilling as the coasters and thrill rides that rival theme parks and regional amusement park operators are adding, but it can invest in the richly themed experiences that make Disney's gated attractions unique.

Isn't that what it's doing here with the drones? Isn't Disney going where no rival has gone before or likely to go in the near future? Cedar Fair (FUN) and Six Flags (SIX) aren't going to be investing in unmanned aircraft vehicles to entertain folks clicking through their turnstiles. They can't. They don't generate the annual attendance and revenue per customer to justify the tech expense.

They will be watching all the same. Disney is under no obligation to go through with its drone dream, but it doesn't make sense to back down after having come this far. This investment in technology will be able to deliver unique entertainment that can be modified quickly and cheaply to provide fresh applications. It's not just Peter Pan or Dumbo that will be flying at Disney's theme parks, and with that comes the family entertainment giant's even bigger dream of flying itself.

Motley Fool contributor Rick Munarriz owns shares of Walt Disney. The Motley Fool recommends and owns shares of Walt Disney. Try any of our Foolish newsletter services free for 30 days.

ShutterstockThey say two thousand zero zero party over, oops! Out of time!

So tonight we gonna party like it's 1999!

-- Prince, "1999"

There is a saying in fashion that "if you wait long enough, everything comes back in to style." Though acid-washed jeans and Day-Glo shirts have yet to become trendy again -- thank goodness -- several stock darlings from the '90s that have been out of fashion for quite some time are now making a comeback.

When the dot-com bubble burst in 2000, many of the previous decade's high fliers took so much damage that they were given up for dead. For example, Microsoft's (MSFT) stock, which had gone up 11,800 percent in the previous 10 years, spent the 10 years following the crash basically going sideways -- aka dead money.

The same fate befell other '90s darlings like Oracle (ORCL) and Intel (INTC). It was common belief in professional investing circles that these once-hot companies had transitioned into more mature phases with slower growth and a corresponding flat stock price.

The Market's Up, and So Are They

However, with a multiyear bull market in full swing and the indexes hitting all-time highs, some of these left-for-dead '90s stocks seem to be staging miraculous resurrections.

For example, Oracle and Microsoft are within 7 percent and 13 percent of their respective all-time highs, both of which were set in late 2000. These numbers are particularly impressive given that post-bubble Oracle had lost 85 percent of its value and Microsoft 72 percent of its value.

Intel might be starting to move to its dot-com highs -- it's breaking into 12-year highs. Qualcomm (QCOM) is another stock from the decade that brought us grunge that has risen from the ashes. After losing almost 90 percent of its value by 2002, it is now within 19 percent of its all-time highs.

There is however another reason -- aside from the general bullish market -- that these stocks have been performing so well, and it's something all investors should pay attention to.

There's a Great Future in Diversification

In the '90s, Microsoft was primarily known for its computer operating system. That is where the vast majority of its sales and profits came from and one of the reasons its stock performed so well. But once it had saturated that market, there didn't seem to be much growth potential left.

But things have changed. Now Microsoft is a major player in the enterprise service business, an area that analysts think could see massive growth. It is also a player in online gaming with Xbox, as well as in VOIP with Skype. In essence, it has a number of technologies and products poised to drive revenues going forward in the same way Windows did in the '90s.

This is the type of transformation that investors want to look for in a company: a company throwing off consistent revenue with a strong bread-and-butter product line and moving into other areas that may reignite earnings growth, and by extension, stock price.

Beam Us Aboard, Scotty

A great example of this is Cisco (CSCO). Once primarily thought of as a provider of routers and switching equipment, Cisco is now rapidly moving into next-generation products such as high-def video conferencing and real-time traffic management systems.

Illustrating this forward-looking approach CEO John Chambers was recently quoted by the Wall Street Journal as saying, "As video moves to the Internet, it's time to have a 'Star Trek' experience. And so I said to my engineering team: I want this to be like 'Star Trek', and I want to be like Scotty."

Cisco is still 66 percent off its 2000 highs, but an approach like the one Chambers is taking to product development may reignite earnings growth at the company, allowing its stock price to catch up with some fellow members from the Class of 1999.

www.elpolloloco.com

One of this year's hottest initial public offerings is a quick-service restaurant chain that prides itself on its grilled citrus-marinated chicken. El Pollo Loco (LOCO) has seen its stock more than double since it went public at $15 in July.

The California-based eatery had its first chance to impress investors with its first quarterly report as a public company on Thursday. It didn't disappoint.

Sales inched 6.3 percent higher to $86.9 million, fueled primarily by a 5.4 percent increase in system-wide comparable-restaurant sales. Adjusted earnings climbed 10 percent to $6.1 million -- or 16 cents a share. The results were in line with analyst targets of 16 cents a share in net income on $86.4 million in sales.

This isn't the kind of monster growth that investors associate with stocks that double within two months of storming out of the IPO gate, but El Pollo Loco now has the ammo to begin expanding its reach beyond the 401 locations open at the end of June. For investors, El Pollo Loco offers an opportunity to cash in on the fast-casual trend that's been faring better than traditional fast-food chains or casual-dining establishments.

Spreading Its Wings

Going public has its challenges. It forces companies to live up to Wall Street's quarterly expectations, and that can often get in the way of carrying out long-term growth plans. However, trading publicly gives a company the ability to tap equity markets to raise capital. It also helps validate brands, and that's a pretty big deal for a consumer-facing restaurant operator that relies on third-party franchisees to help build out its empire. A majority of its eateries -- 233 locations, or 58 percent -- are owned and operated by franchisees.

Expansion has been slow until now. El Pollo Loco had 347 locations when it originally tried but ultimately failed to go public in 2006. Growing your store count by 16 percent through eight years isn't very impressive.

El Pollo Loco had 398 restaurants open a year ago. It has added only one company-owned location and a pair of franchised outlets to get to 401 today. The pace should intensify at this point. El Pollo Loco's IPO proceeds went to pay down debt, but that still gives it more financial freedom than it had over the past year, when it saw its store tally expand by just three locations. It's hoping to open as many as 11 company-owned eateries this year, with franchisees opening another four.

As long as store-level sales continue to hold up -- and that's just what El Pollo Loco sees for the balance of 2014 -- it should hold up well.

Heating Things Up

El Pollo Loco's success comes at a time when other recent restaurant debutantes are taking a step back. Potbelly (PBPB) went public at $14 late last year, also more than doubling shortly after its IPO. A few disappointing quarters later, the sandwich baker is now trading in the pre-teens, below its original IPO price.

Noodles & Co. (NDLS) also was a hot plate special last year, trading north of $50 shortly after the pasta boiler's market debut. A few quarterly duds later and the stock is down to the high teens.

All three chains initially drummed up investor interest as fast-casual concepts. Eateries that offer diners the convenience of fast food but with quality commensurate with casual dining have scored well with hungry patrons and even hungrier investors. However, Potbelly and Noodles & Co. proved mortal. El Pollo Loco held up well in its first quarter since going public. It's encouraging to see it come through with strong comparable-restaurant sales during the same period that Potbelly and Noodles & Co. clocked in with negative comps. El Pollo Loco will need to keep it coming. If its less-fortunate fast-casual peers have proven anything, it's that the market can spit you out if you lose your flavor.

Motley Fool contributor Rick Munarriz and the Motley Fool have no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. For info on promising dividend stocks, check out our free report.

The funding status and levels of U.S. pensions is heading the wrong way. Despite a rising stock market, a report from the BNY Mellon Investment Strategy and Solutions Group is signaling that the funded Status of U.S. corporate pensions fell to 90.1%. On the flip-side, public pension plans, foundations and endowments gained in August. The biggest issue at hand still seems to be incredibly low interest rates. These keep pension funds from being able to meet certain income targets.

The funding status and levels of U.S. pensions is heading the wrong way. Despite a rising stock market, a report from the BNY Mellon Investment Strategy and Solutions Group is signaling that the funded Status of U.S. corporate pensions fell to 90.1%. On the flip-side, public pension plans, foundations and endowments gained in August. The biggest issue at hand still seems to be incredibly low interest rates. These keep pension funds from being able to meet certain income targets.

In the days leading up to the official opening of the most ambitious expansion in the park's history, Disney's blog teased about dragon sightings, culminating in an

In the days leading up to the official opening of the most ambitious expansion in the park's history, Disney's blog teased about dragon sightings, culminating in an