Brynn Anderson/APTens of millions of Americans are expected to travel this holiday weekend.

NEW YORK -- Turkey, stuffing and a helium-filled Thomas the Tank Engine were on the menu as friends and families gathered across the United States to celebrate Thanksgiving.

Here's a look at how Americans prepared to celebrate Thanksgiving.

Giants in the Sky

The nationally televised Macy's Thanksgiving Day Parade will include six new giant balloons including Thomas the Tank Engine, Paddington bear and the Red Mighty Morphin Power Ranger. The annual event brings out throngs of people along its midtown Manhattan parade route, ending in front of the store's flagship location.

On Wednesday, passers-by on the Upper West Side got a sneak preview, as the giant balloons were inflated with helium in the neighborhood around the American Museum of Natural History.

"It's really cool, they're huge," said San Francisco resident Ella Missan. Daisy Elliot of Boston, who said she's been coming to see the balloons since she was little, agreed. "It's really exciting for me to see the balloons year after year," she said.

The parade's executive producer, Amy Kule, said organizers were glad wintry weather that made sidewalks slick and travel treacherous on Wednesday was expected to be gone by Thursday.

"We're suffering through a little bit of this now but the end result is really going to be a beautiful parade," she said.

Travel Troubles

Rain and snow on Wednesday made getting around on one of the busiest travel days of the year a chaotic experience for some. The sloppy mixture caused hundreds of flights to be grounded in the Northeast.

Some travelers tried to beat the storm by flying out earlier, and airlines tried to be helpful by waiving re-booking fees. But many flights already were filled, leaving travelers with few options.

The roads weren't much better. By midafternoon, the line between rain and snow went along Interstate 95, the major roadway connecting Boston to Washington, and accidents abounded. Snowfall totals were expected to be as much as 6 to 12 inches in the higher elevations west of I-95.

The AAA estimated that 41.3 million travelers would be on the road between Wednesday and Sunday. That's up 4.3 percent from last year.

Holiday Shopping

To the delight of some and consternation of others, it's increasingly become commonplace to see stores open on Thanksgiving, as retailers try to entice shoppers inside and kick off the holiday shopping season a day earlier than the traditional Black Friday. Some of the stores open for at least part of the day on the holiday include Kmart, Target, Sears, Macy's and Wal-Mart. Other stores, like Neiman-Marcus, Nordstrom and Costco, are closed.

Jean-Marc Giboux/AP Images for KmartBy ANNE D'INNOCENZIO

NEW YORK -- Millions of Americans are expected to head to the stores for holiday gift shopping on Thanksgiving in what's quickly becoming a new holiday tradition.

By 4 p.m. on Thanksgiving, 100 shoppers were in line at the Toys R Us in New York City's Times Square.

Mary Smalls, 40, was one of those waiting for the store's 5 p.m. opening. She plans to get all her shopping done on Thanksgiving to avoid heading out on the day after the holiday known as Black Friday.

"I'm going to try to avoid the crowds," said Smalls, who plans on spending $300 or $400 on gifts this year.

Just a few years ago when a few stores started opened late on the holiday, the move was met with resistance from workers and shoppers who believed the day should be sacred.

Last year, more than dozen major retailers opened at some point on Thanksgiving evening. And this year, at least half of them -- including Target (TGT), Macy's (M), Staples (SPLS) and J.C. Penney (JCP) -- are opening earlier in the evening on the holiday.

The Thanksgiving openings are one way retailers are trying to compete for Americans' holiday dollars. Used to be that Black Friday was when they'd focus their sales promotions. But increasingly, they've been pushing those promotions earlier on Friday -- and eventually into the holiday itself -- to grab deal-hungry shoppers' attention.

Bill Martin, co-founder of ShopperTrak, which tracks data at 70,000 stores globally, is expecting a sales increase of 3 percent to 5 percent to $2.57 billion to $2.62 billion on Thanksgiving. Last year's figure grew two-fold from the year before.

The National Retail Federation expects 25.6 million shoppers to take advantage of the Thanksgiving openings, down slightly down from last year.

Kathy Grannis, a spokeswoman at the retail trade group, said that earlier promotions in the month and shoppers' uncertainty about when they can get the best deals are factors that could lead to fewer shoppers coming out on the holiday.

Nevertheless, Thanksgiving is starting to take a bite out of Black Friday business. Indeed, sales dropped 13.2 percent to $9.74 billion on Black Friday last year. Analysts said Thanksgiving sales were in part responsible for the decline.

And Gerald Storch, who runs a retail consultancy called Storch Advisors, said stores that open on Thanksgiving get more of their share for the weekend than others who open on Friday.

"That's why they keep doing it," he said. "You have to be first."

Being first lures shoppers like Fred Peek of Atlanta. He plans to shop on Thanksgiving at Best Buy (BBY) or Walmart (WMT) for a camera. Peek said that with more stores opening for a longer period of time on Thanksgiving, he believes shopping will be less hectic that last year.

"It won't be such a rush trying to get to where I need to get to," he said.

Not every store is opening on Thanksgiving, though. Some, including GameStop (GME), Costco (COST) and Ikea, have said they won't open because they want their workers to enjoy the holiday with their families.

"At GameStop, we often use the phrase 'protect the family' in reference to our business," the video game retailer said in a company statement.

And not every shopper is happy about stores opening on the holiday. A number of petitions have been circulating on change.org targeting Walmart, Target and other retailers for opening their stores on Thanksgiving, or starting their sales that day. Most of Walmart's stores already open around the clock.

-AP Business Writer Damien Troise in New York contributed to the report.

djuggler/Flickr

One of last week's biggest losers was Pandora Media (P), shedding nearly 10 percent of its value after disruptive peer-to-peer taxi service Uber struck a deal with Spotify and media reports suggested that Apple (AAPL) was intensifying its digital music efforts.

Consumer appetite for streaming music is growing, and Pandora is still the top dog. This would seem to make it a natural beneficiary of the trend, but some things aren't working out so swimmingly for Pandora investors. The stock has shed more than half of its value since its springtime peak, and the marketplace is starting to get a lot more competitive.

The Uber Challenge

Uber has been making waves as the new way for car-less folks to get around. Instead of hailing a cab or dealing with the lengthy delays of mass transit, people who need to get somewhere can fire up the Uber app and have a registered driver come over and take them there for less than the conventional cab fare.

Uber announced earlier this month that it's teaming up with Pandora rival Spotify to allow that music service's premium subscribers to play the tunes they want to hear through their driver's stereo. All they need is an iPhone or Android smartphone with Bluetooth functionality. The offering rolled out in 10 Uber markets.

Pandora has tried to get its integration in cars, but it could never let folks pick out the actual tracks they want to hear on a drive as a passenger. Unlike Spotify, where users single out the exact songs they want to hear, Pandora is a music discovery engine that plays similar tunes based on the user's input.

In theory, the Uber deal with Spotify is a small deal. Just a quarter of Spotify's 40 million users are premium subscribers, and some would argue that many of those folks already have cars. However, it's just one more way that a Pandora rival is standing out in this heated climate.

Growth at Pandora, after all, is slowing. Its active user base has only increased 5 percent to 76.5 million over the past year, and is practically unchanged from the 76.4 million active listeners it had on its rolls just three months earlier. Pandora users are listening more, and it's commanding higher ad rates. However, the future is going to get more cutthroat than the past.

An Apple a Day

London's Financial Times reported last week that Apple will bundle its fledgling Beats Music service into its iOS operating system, according to people familiar with the situation. Apple was the original leader of the digital music revolution with its iTunes app and storefront. However, as the way we consume music has changed -- we prefer to stream a wide catalog of music instead of owning a handful of tunes -- the consumer tech giant has been trying to catch up.

The first step came last year when Apple introduced the Pandora-like iTunes Radio. Earlier this year it acquired premium headphones maker Beats Electronics, and with that came the Spotify-like Beats Music platform that rolled out earlier this year.

In other words, Apple is about to throw some muscle behind music discovery and on-demand streaming.

Pandora is still cool. It's still popular. However, its inability to turn its users into paying customers -- there were just 2.5 million of those as of early last year -- has cast it as an ad-supported platform for freeloaders. With user growth slowing and the competition getting smarter, one has to wonder if Pandora is peaking in popularity, just months after its stock appears to have done the same.

Motley Fool contributor Rick Munarriz is no stranger to digital music. His bandParis by Air can be heard on Spotify and iTunes, but he's not quitting his day job. He has no position in any stocks mentioned. The Motley Fool recommends and owns shares of Apple and Pandora Media. Try any of our Foolish newsletter services free for 30 days. Check outour free report on the Apple Watchto learn where the real money is to be made for early investors.

If the past year has taught consumers anything, it's that identity thieves, fraudsters and scammers are on the prowl, going after any information they can use to make a buck. But the intrusions don't stop there. If the thought of being the unwitting star of your own prime time reality show gives you the willies, consider the recent revelation that more than 73,000 unsecured webcams and surveillance cameras are, as I write this column, viewable on a Russian-based website. The site lists the cameras by country. (Unfortunately, the U.S. is well represented.)

In every case, victims ignored safety protocols and installed the cameras with their default login and password-admin/admin or another easy-to-guess combination findable on any number of public-facing websites. According to NetworkWorld, "There are 40,746 pages of unsecured cameras just in the first 10 country listings: 11,046 in the U.S.; 6,536 in South Korea; 4,770 in China; 3,359 in Mexico; 3,285 in France; 2,870 in Italy; 2,422 in the U.K.; 2,268 in the Netherlands; 2,220 in Colombia; and 1,970 in India. Like the site said, you can see into 'bedrooms of all countries of the world'. There are 256 countries listed plus one directory not sorted into country categories."

Why It Matters

You may remember the sextortionist who hacked into Miss Teen USA's computer camera and took compromising photographs. He tried to get money in exchange for not distributing the pictures, and got 18 months behind bars instead. That's a bit too lenient in my book. Unfortunately, there are thousands more slime-balls where these guys came from who are poking around, looking for ways to exploit the private moments of your life for their personal amusement or gain.

The Internet of Things has arrived making homes smart, fitness totally interactive and tasks infinitely easier, but the devices we buy to streamline day-to-day life create vulnerabilities that, when exploited, could bring your day to a screeching halt, and the risks are much higher if you don't apply common sense during the setup of these password-protected devices. The rule here couldn't be simpler: Anything that hooks into a network must be locked down.

Don't think it will happen to you? Consider this: There are websites that list the default passwords of all kinds of devices. If you have something wireless that's hooking up to your household router, it likely came with a pre-set password and login. And there's a good chance, whatever the device, there's a forum online where it's been figured out, hacked, cracked and hijacked for all stripe of nefarious purpose.

Convenient ... for Everyone

The added convenience provided by the Internet of Things is obvious, but the security issues may not be. Are your fitness records hackable by a third party? Are they linked to social media? How much information did that require? A login? A password? And what's to stop a hacker from opening your front door or turning off your heat during a blizzard or your lights during a home invasion: all with an app?

Other common devices that are password protected should immediately come to mind here. Whether it is your household printer, your wireless router or your DVR, there are folks out there who are curious about you, not because they value you as a human being, but because they can create value from any plugged-in human-whether by fraud or extortion or (in a more old-fashioned mode) getting the information they need to rob you blind when you're not home.

The number of people who don't change default passwords is staggering, as evidenced by the 73,000 wide-open webcams on that Russian website. There's a major disconnect here, and it's specific to the Internet of Things. On the Internet proper, it seems the message has finally seeped in and people are beginning to make themselves harder targets -- making sure their privacy settings are tight and their passwords are both strong and changed frequently.

But when it comes the Internet of Things, there is still more learning to be done -- hopefully not Miss Teen USA-style. The solution, for this particular problem, is remarkably simple: Set a long and strong password on all devices. Whatever it is, it's your job to pick something easy for you to remember and hard for others to guess.

The Bigger Problem

The Pew Research Center released a statistic this month that showed 90 percent of Americans believe they have no control over their personal information-that the facts and figures and ciphers unique to them are simply in too many places, and essentially that the data cat's out of the bag.

Breaches have crossed the Rubicam. Whether they are of the unavoidable variety or the product of carelessness, they will continue to happen apace. Now the third certainty in life, breaches have become the potholes on a bumpy road. What no one wants to deal with is the fact that the road ends abruptly -- jagged concrete and rebar sticking out -- and there's nothing but air after that, and a whole lot of it, between you and the endless crimes that can be committed against you.

Adam Levin is co-founder and chairman of Credit.com. This post does not necessarily represent the views of Credit.com or its partners.

Workers who held jobs in both the private and public sectors over their careers could be in for a shock when it comes time to claim Social Security. If you get a government pension, the Social Security benefit that you earned from your private job could be slashed by hundreds of dollars a month.

That came as a big surprise to Jim Knight, 68, of Vallejo, California, who filed for his Social Security benefit at age 66. He had paid into the system in the years before he took a public teaching job. "I had earned my credits," says Knight, which provided him a Social Security retirement benefit of about $1,000 a month. But a year ago, Knight started getting his teacher's pension check and his monthly Social Security benefit dropped to $600. "It's unfair. That money is mine," he says.

Windfall Elimination Provision, Government Pension Offset

Knight was hit by what's known as the windfall elimination provision. This provision affects workers who have had two careers: private-sector jobs that were covered by Social Security and state or local government jobs that were exempt from the Social Security payroll tax.

Many public pensioners get hit twice. If they apply for a Social Security spousal or survivor benefit based on a spouse's earnings record, those benefits will be reduced as well -- and possibly eliminated. That rule is known as the government pension offset.

The windfall provision does not apply to public pensioners who have 30 years or more of substantial earnings under Social Security. And Social Security benefits are not reduced for those with military pensions.

The windfall provision was aimed at correcting a quirk in the calculation of Social Security benefits. Benefits are based on average monthly earnings and are meant to replace only a percentage of a worker's salary. The formula replaces a greater percentage of a lower-wage worker's salary than it does a higher-wage worker's salary.

Congress Changed the Rule

Until the early 1980s, the Social Security Administration assumed that workers who had zero annual earnings for a certain number of years were low-wage workers -- even though they may have received paychecks from public jobs. In 1983, Congress approved a new formula to end this "windfall."

Say a person worked for 10 years in the private sector at $50,000 a year and drew a public pension of $2,500 a month. If the windfall provision did not exist, she would receive a Social Security benefit of $894 a month at age 66. But under the provision, her benefit is $487. (The maximum windfall reduction for 2014 is $408.)

The windfall provision also affects a Social Security spousal benefit based on the public pensioner's earnings record, says Jason Visner, a financial adviser for Brook Capital, in Brookfield, Wisconsin. In this example, the pensioner's spouse would qualify for a spousal benefit of up to half of $487, instead of half of $894. A surviving spouse, however, will get the pensioner's full Social Security benefit without the windfall reduction.

A Hit on Spousal and Survivor Benefits

The public pensioner who applies for a spousal or survivor benefit based on a spouse's Social Security earnings record also faces reductions. Usually, a spouse gets up to 50 percent of a worker's Social Security benefit, and a survivor gets up to 100% of the worker's benefit.

The pension offset reduces the spousal or survivor benefit by two-thirds of the public worker's pension amount. Say your late spouse worked his entire career in the private sector and had a Social Security benefit of $2,500 when he died. If you're getting a public pension payment of $2,000 a month, your Social Security survivor benefit will be $1,167. (That's $2,500 minus $1,333, which is two-thirds of $2,000.)

The pension offset was meant to keep benefits in line with Social Security rules covering private workers. A beneficiary, for instance, is not entitled to claim both her full retirement benefit and a full spousal benefit. So if a beneficiary is entitled to a retirement benefit of $800 and qualifies for a spousal benefit of $1,000, she gets her $800 benefit plus $200 of the spousal benefit.

Make Some Calculations

Still, those hit by both say the formulas are arbitrary. "The figures are not based on reality. It was political football," says retired teacher Bonnie Cediel, whose group Social Security Fairness wants Congress to repeal the provisions.

Don't expect a fix anytime soon. In the meantime, you can find out whether you'll be subject to either and determine how they could affect your retirement income. "If you don't know that's coming, you're in for a rude awakening," Visner says.

Check your Social Security statement, which you can find online if you sign up for a "My Social Security" account at www.socialsecurity.gov. Zeros will show up in years in which your earnings came from a job that wasn't covered by Social Security. You can calculate the impact on your benefit by using the site's WEP calculator. To estimate your monthly Social Security benefit, plug into the calculator your earnings from years of private work, zeros for your years of public-sector earnings and your monthly public pension benefit.

The windfall provision will take a bite from your Social Security benefit no matter when you claim. But if you claim before full retirement age, your benefit will be reduced both by the windfall provision and for claiming early. If you wait until 70, you'll still be hit by the windfall provision, but you'll get an 8 percent delayed retirement credit for each year you delay past your full retirement age.

Would a Delay Help?

Those rules in part are motivating Michael Medaglia, 64, and his wife, Denise, 63, of Groveland, Massachusetts, to consider delaying their Social Security benefits. Denise retired three years ago as a public school teacher. She receives a public pension and is also eligible for a small Social Security benefit. Michael is still working full time in the private sector.

Even with a delay, the windfall provision slashes Denise's benefit, and the pension offset reduces any spousal or survivor benefit she would get on Michael's record. But the survivor benefit would be larger if Michael delays. "It makes good economic sense to defer as long as we can," he says.

For couples who want to maximize benefits, delaying could also make sense if the higher-earning spouse's Social Security is slashed by the windfall provision. Say the higher earner at 66 has a $1,500 monthly benefit but it's reduced to about $1,100 a month. Meanwhile, his lower-earning spouse has her own $1,200 benefit. Because the windfall provision doesn't slash the survivor benefit, the lower earner could get a $1,500 survivor benefit if she outlives the higher earner. And if the higher earner delays his benefit to age 70, the survivor benefit will be $1,980.

The end of the year is hectic for most of us; we are juggling parties, holiday shopping, travel, and spending time with family and friends. The last thing we want to right now do is think about money. That's what New Year's resolutions are for, right?

While it's tempting to put off your finances until the New Year, you might miss some critical financial deadlines and face penalties or lose the opportunity to save extra money. An end-of-year financial checklist gives you the opportunity to make changes and save some serious dough before the clock strikes midnight on Dec. 31.

Getty Images"Women deserve equal pay for equal work."

-- President Barack Obama, 2014 State of the Union address

That may seem obvious, but unfortunately, equal pay regardless of gender is still far from reality in America -- a fact that women, of course, are not thrilled with. In fact, according to a recent poll by Gallup, more than anything else work-related, women in the U.S. workforce today want better pay.

Ever since World War II, women have represented a larger and larger proportion of the U.S. workforce. Over the past five decades, women have grown their representation in the labor pool by roughly 50 percent. According to Labor Department statistics, in 1960, about one in three workers in the U.S. was female. At last report, in 2010, that number had grown to nearly one in two (47 percent).

Pay for women workers has also improved. For every $1 in wages that a male worker earned in 1960, a woman working an equivalent job would have earned about 61 cents, according to the U.S. Census Bureau. By 2009, the Bureau says, that number had risen to 77 cents -- and more recently, according to the Department of Labor in 2013, to 81 cents.

So the gap has narrowed, but there's still a gap.

What Women Have, and ...

Surveying 2,076 full-time workers ages 18 and up from 2010 to 2014, Gallup discovered that by and large, women are happier with how the workplace "works" for them than men are. For example, 65 percent of women say they are satisfied with the flexibility of work hours offered to them at their job, 60 percent find their employer's vacation policy acceptable, and 50 percent say they receive recognition from their boss for their work.

In each case, these scores are 4 percentage points higher than what male workers told Gallup about their own satisfaction at work. Statistically, that's on the outer edges of what Gallup says is the survey's margin of error -- plus or minus 4 percent -- and thus Gallup confides that these scores are therefore "not statistically significant." But it sure sounds significant.

More questionable given the margin of error, but still worthy of notice, are Gallup's findings that women are 2 percentage points (54 percent) more likely than men to be satisfied with their "job security," and 2 percentage points (57 percent) happier with their bosses as well.

Both genders cite "physical safety conditions" as the workplace factor they're most pleased with -- but here, too, women are happier than men, albeit by a single percentage point (74 percent versus 73).

What Women Want

In only three categories covered by Gallup's poll do women appear less pleased with their work environment than men are: job stress, promotion opportunities, and ... pay. And as it turns out, pay is the real sticking point. (In fact, it's the single category in the survey for which Gallup is certain about the statistical significance.)

According to Gallup, women express "complete satisfaction" with the amount of money they're earning at a lower rate than men do -- 6 percentage points lower. And the satisfaction gap may be even bigger than it looks.

Consider: The percentages of women (and men) expressing complete satisfaction with their pay is already pretty small (28 percent of women versus 34 percent of men). So looked at another way, that's a bit more than one woman in four, versus one man in three, saying they're completely satisfied with their pay. Statistically speaking, that means women are only 82 percent as likely to say they're completely happy with their pay as men are.

Eighty-two percent. Coincidentally, that's almost the exact same number the Labor Department cites for the percentage of pay a woman gets today compared to the wages of a man doing the same job.

Go figure.

Motley Fool contributor Rich Smith is a man, and prefers to avoid raising the subject of the wage gap at cocktail parties. He also prefers to avoid attending cocktail parties. To read about our favorite high-yielding dividend stocks for any investor, check outour free report.

Human compassion may be woefully absent on Black Friday and Cyber Monday, but it's set to bounce back the following Tuesday stronger than ever.

#GivingTuesday is expected to smash old records for charitable donations as it has each of the last two years, a result of the marketing and social media muscle surrounding the event.

"The number of dollars raised is really important," Curran said, emphasizing that the founders of the movement want to see all charitable groups succeed in their fundraising goals. "But I think that seeing people talk about giving in a whole new way and seeing them talk about it all kinds of different contexts and in all kinds of different geographic locations is equally meaningful."

That conversation itself speaks to #GivingTuesday's success in answering a deeper human need. Like the famously viral ice-bucket challenge, #GivingTuesday offers people an opportunity to do good in any way they can. That impact can be impossible to measure but hints of it exist in real dollars, as donations to the charities that carry the torch of our concern for one another have shot up in the last two years.

According to The NonProfit Times, donations on #GivingTuesday in 2013 amounted to $32.33 million processed on five online platforms: Blackbaud, PayPal, Razoo, Network for Good and DonorPerfect. Blackbaud, which handles contributions for large nonprofits, reported that it processed $19.2 million in online donations on the day, a 90 percent increase over the prior year. Blackbaud also reported the average donation it processed rose by 40% in 2013 to $142 from $102 in 2012.

16,000 Partners

#GivingTuesday had more than 2,500 partner entities in 2012. That shot to more than 10,000 global partners in 2013 and greater than 16,000 partners in the U.S. and more globally.

Quoted in The NonProfit Times, Blackbaud's director of corporate citizenship and philanthropy Rachel Hutchisson said #GivingTuesday "didn't just borrow. It didn't take people's giving on Dec. 31 and have it happen earlier. The data strongly suggests that #GivingTuesday was additive" to most groups' fundraising efforts.

In addition, the event has caught fire beyond U.S. borders, where it is often more about community service and caring than about dollar donations. In the U.S., a big part of #GivingTuesday's appeal is as an antidote to the rampant consumerism of the biggest U.S. holiday shopping weekend of the year. But its popularity overseas proves it is more than that.

"Global expansion has been really inspiring, especially because it shows that creating a shared day for giving has a role in places where Black Friday and Cyber Monday don't even exist," Curran said, emphasizing that the invitation to help one another strikes an important chord in people everywhere. "A lot of those global examples are not based around fundraising, but are entirely volunteer efforts," she said.

More Mentions on Social Media

Designed from the outset to be a decentralized movement rather than a PR campaign led by 92Y, #GivingTuesday last year outstripped Cyber Monday for mentions on social media, Curran said. "People really taking it on themselves to spread the word."

High-powered backers have lent important support, like #GivingTuesday co-founder the U.N. Foundation and the White House. Between 15 percent and 20 percent of Americans are aware of it. As the word spreads, companies, nonprofits and individuals are starting to flock to the #GivingTuesday campaign.

Hyatt Hotels (H) signed on this year, using the event to raise awareness of its community grants program, where 31 grants worth between $5,000 to $20,000 are donated to organizations in communities where its hotels are located, nominated by local staff.

H&M department stores has launched an effort to donate $7.5 million worth of clothing to people in need, in partnership with K.I.D.S./Fashion Delivers, an organization that delivers donated clothing to more than 800 charities. H&M is also using the day to raise money through in-store donations to K.I.D.S./Fashion Delivers.

Crowdfunding site IndieGogo this year offered reduced fees and added support for customers participating on its platform for their own #GivingTuesday campaigns. Currently the site has 175 active #GivingTuesday-branded campaigns, with a total raised so far of $5.5 million.

Discover (DFS) has pledged to add 2 percent to all cashback bonus donations and donations made with Discover to its cashback bonus charitable partners. Discover will also add to its employees' donations to any charity on Dec. 2.

Microsoft (MSFT) , an important early partner for #GivingTuesday, has been building its involvement, ramping up its activities each year. This year, the company's YouthSpark #GivingTuesday campaign is reaching out to U.S. and international organizations listed on www.globalgiving.org and www.globalgiving.co.uk, offering $350,000 in funds to match up to $500 per donor per project.

One of the more exciting aspects, Curran said, is state governments using #GivingTuesday. Maryland's participation grew out of Baltimore's 2013 #GivingTuesday campaign, which raised more than half a million dollars beyond its goal. Such activity "shows me that these campaigns are not only great in and of themselves, but they have a great opportunity to scale," she said.

DES MOINES, Iowa -- Christmas tree likely will cost a little more this year, and growers like John Tillman say it's about time.

Six years of decreased demand and low prices put many growers out of business. Those who withstood the downturn are relieved they survived.

"I'm awful proud to still be in the Christmas tree business," said Tillman, who ships up to 20,000 trees each fall from nine fields south of Olympia, Washington. "We lost a lot of farmers who didn't make it through."

Prices vary according to the variety of tree, but growers this year will see about $20 per tree, $2 more than the last several years, according to Bryan Ostlund, executive director of the Salem, Oregon-based Pacific Northwest Tree Association. Prices will likely rise as the holidays near and supply decreases.

Consumers looking to deck their home could pay a little more than last year, but costs vary widely depending on factors such as transportation, tree-lot rental space and big-box retailers' demand that prices remain stable. For example, a 6-foot Douglas fir in Oregon, which grows about one-third of the nation's Christmas trees, could sell for $25 while a similar tree hauled to Southern California might go for $80.

Tara Deering-Hansen, a spokeswoman for Midwestern supermarket chain Hy-Vee, said wholesale tree prices have climbed slightly but prices are set at each store and customers might not see any increase.

Heavy snow last week slowed the shipment of trees from Michigan, which ranks third in production and supplies much of the Midwest and parts of the South. In some loading yards, stacks of trees awaiting shipment were covered with up to 2 feet of snow.

"Getting the snow off was more work than loading the trees," said Dan Wahmhoff, co-owner of a nursery in southwestern Michigan. "It was definitely a challenge -- wind and snow and cold, trucks were getting stuck -- but we made it through."

In the coming years, growers expect the supply of trees to remain stable with prices gradually increasing, in part because it takes six to seven years for a seedling to grow large enough to sell.

Even with the increase, most growers are being paid less now than in the mid-2000s, when trees from new and expanded farms hit the market as demand fell. And the industry still faces challenges, as competition from artificial tree manufacturers and other factors have led to a drop in trees harvested, from 20.8 million in 2002 to 17.3 million in 2012, according to the U.S. Department of Agriculture.

The National Christmas Tree Association, based in Missouri, has encouraged growers to offer more options that meet the needs of younger people who live in urban areas and don't have space for a towering tree, says executive director Rick Dungey. More growers are realizing that if they offer different looks -- such as a tree that could fit on a coffee table or one thin enough to squeeze into a narrow room -- people will buy them, Dungey said.

"There are more options and choices out there," he said.

Small tree-farm owners who sell straight to customers aren't as affected by the factors increasing prices to consumers nationally.

Jenny Howell, whose family runs Howell Tree Farm southwest of Des Moines, said they'll raise prices a bit because of high fuel prices for mowers and other equipment over the summer and drought that caused some seedlings to die. But their customers typically return each winter and don't spend time comparing her farm's prices to those in city lots.

It can be cold, hard work traipsing through the snowy tree farm in December, but Howell said her family still enjoys it.

"It's a happy business," she said.

-Associated Press writer John Flesher in Traverse City, Mich., contributed to this story.

Being self-employed has major appeal, such as the financial freedom to expand your business on your own terms; opportunity for partnerships or acquisition; and the freedom to wear pajama bottoms all day. However, it's not all wine and roses -- or coffee and flannel -- for that matter. You're the boss now, and no one is going to take care of you but yourself. There are some major mistakes that could be made, and failing to plan adequately for retirement is one of them.

According to a recent TD Ameritrade survey, nearly 70 percent of America's 10 million self-employed workers aren't saving regularly for retirement, and 28 percent aren't saving at all. Those are some frightening numbers, but not nearly as terrifying as entering retirement without any savings to support you.

If you are self-employed, squeezing extra money out of your budget can be tough. Your income might be unpredictable and cash flow might be tight. It can be hard to prioritize retirement when you are trying to build a business, and the various retirement plans can be overwhelming. Consider these:

Solo 401(k)

A solo 401(k), also known as an individual 401(k), is a one-participant 401(k) plan; you are the administrator and the contributor. Contributions are made on a pre-tax basis and you can contribute up to $17,500 for 2014, with an additional $5,500 in catch-up contributions if you are over 50 years old. This plan is best for self-employed people with high incomes and no other employees (except a spouse), or older self-employed people who are behind in their retirement saving and need to catch up.

What makes these plans particularly appealing is that in addition to the $17,500 maximum contribution, you can also contribute up to 20 percent of your net self-employment income. If your spouse is an employee (he must work for the business and be paid a reasonable salary), he can also contribute the same amount, essentially doubling your investment. Finally, for self-employed people who receive an inheritance or windfall, a solo 401(k) can act as a tax shelter.

There are some drawbacks: You can contribute to an employer's 401(k) and a solo 401(k) at the same time but your total contribution match is still $17,500 - you can't max out both plans. You can still contribute up to 20 percent of your net self-employment income the solo 401(k), but your contributions can't exceed your self-employment income for the year. Also, if you hire employees other than a spouse, you are no longer eligible for a solo 401(k) and will have to covert it to a regular 401(k). Finally, if your solo 401(k) has over $250,000 in it you will have to go though the hassle of filling out additional paperwork with the IRS.

Solo 401(k) plans are offered by most major financial firms and are fairly easy to set up. You can withdraw from a solo 401(k) under certain circumstances but not all firms offer this option, so make sure to ask. There is also a Roth version of this plan but you won't get an up-front tax break, although the money will continue to grow (and eventually be withdrawn) tax-free.

Tip: Some financial experts recommend using a separate federal Employer Identification Number for your solo 401(k) to simplify your taxes. You can get one from the IRS website.

Simplified Employee Pension IRA (SEP IRA)

This is perhaps the most simple self-employed retirement plan available: it's a great choice for business owners without employees or moonlighters (regular workers with self-employed income on the side). You can have a SEP IRA if you have employees, but there are strict conditions for an employee to be eligible. The 2014 maximum contribution for a SEP IRA is up to 25 percent of your net self-employment income or $52,000, whichever is less.

The SEP IRA's flexibility is what makes it particularly attractive: you can wait to fund the plan until you file your taxes, in case your income is higher than expected, and then make a larger contribution to avoid a higher tax bill. If you make less than you expected, you can scale back your contribution.

You can also open a SEP IRA any time before your business' tax-filing deadline -- it does not have to be opened before the first of the year. You can also take longer to contribute to your SEP IRA by filing for an extension. Some business owners do this regularly to give themselves more time to contribute money to the plan and maximize the tax benefits.

There are a few disadvantages: The contribution limits of a SEP IRA are lower than a solo 401(k). Remember a solo 401(k) allows you to contribute up to the 20 percent net profit plus an additional $17,500. Also, with a SEP IRA there are no catch-up contributions allowed. So if you are nearing retirement and just staring to save, this might not be the best option for you. Finally, loans from SEP IRAs are not allowed but you can withdraw the money at any time. You will pay penalties, so it's not a decision to take lightly.

Tip: Treat your SEP IRA contribution like a regular bill and schedule automatic payments directly into the plan.

Savings Incentive Match Plan for Employees (Simple IRA)

A Simple IRA is a type of traditional IRA for small business owners with 100 or fewer employees, and the self-employed, with aspirations of growing their businesses. The contribution limits max out at $12,000 for 2014 (plus an additional $2,500 if you're 50 or older). You also cannot maintain any other retirement plans, including SEP IRAs or qualified plans. Unlike the SEP IRA, there is no income restriction - you can put a full 3 percent of your net self-employment income into the plan.

What really makes the Simple IRA stand out is that the employer is required to make a contribution on the employee's behalf in one of the following ways: either dollar for dollar, up to 3 percent of the employee's salary or a flat 2 percent of pay, regardless of whether the employee contributes to the account. You, the employer, will benefit from major tax deductions, both from your own contributions and employee deferrals. You will also have the added benefit of attracting and retaining quality employees.

This might sound a little complicated, but Simple IRA plans really are, well, simple. They are generally easier and cheaper to start up and maintain when compared to qualified plans. Employees can contribute through regular paycheck deductions and are not required to provide annual financial reports.

You can open a Simple IRA between Jan. 1 and Oct. 1 of each year. If you become self-employed after Oct. 1, you can set up a Simple IRA plan for the year as soon as administratively feasible after your business starts. Loans from Simple IRAs aren't allowed but you can withdraw the money at anytime with penalties. The penalties are severe, however: 25 percent if made within the first two years of participating in the plan.

Keogh have now been largely replaced by SEP IRA plans. Until 2001, Keogh plans allowed for larger annual investments than other retirement plans, which is what made them appealing to many business owners. Now, the contribution limits for both Keogh plans and SEP IRAs are the same. The Keogh is also more difficult to set up, and you cannot participate if you qualify as an independent contractor. Keogh plans are still an option for self-employed individuals who own their own unincorporated businesses (sole proprietorships, partnerships and LLCs), but the SEP IRA is usually recommended over this plan.

PepsiCo (PEP) thinks that protein drinks and low-calorie sparkling beverages to counter the slow growth of the U.S. carbonated beverage industry.

"Expect to see from us an interesting number of mid- to low-calorie sparkling beverage platforms," in 2015 said Simon Lowden, Pepsi's chief marketing officer of Pepsi Beverages North America, in an interview with TheStreet. Lowden said that "Tropicana will see news around sparkling juices and waters," while "you will see protein as an ingredient come in across more and more beverages."

Protein could be added to Gatorade, which will come out with more energy chews and bars. Year-to-date volume for Gatorade sports drinks have increased by a mid-single digit percentage.

Coconut water, an industry that ballooned to $400 million in U.S. sales last year, according to research firm Euromonitor, is being targeted in a larger way by Pepsi aside from it leveraging its majority stake in O.N.E. coconut water. O.N.E was third in terms of 2013 annual sales in the coconut water category, behind the privately held Vita Coco and Zico, which is owned by Coca-Cola (KO). "You will see more news from us on coconut water next year as an ingredient across brands like Mountain Dew," said Lowden.

A Focus on Health

The healthy theme that underlies Pepsi's innovation push next year, and also recently at Coca-Cola with its Life product that has 35 percent fewer calories than a typical cola, is meant to counteract demand shifts in the carbonated soda industry. "In the last 18 months, the conversation in the U.S. has gone from 'How many calories am I taking in?' to 'Is it artificial?' "

Pepsi has jumped ahead of Coca-Cola in the race to reignite consumer interest in soda by entering the emerging craft soda industry with its new brand Caleb's Kola.

The naturally sweetened soda in a brown glass bottle is named after Pepsi's founder, Caleb Bradham. Available at Costco (COST) locations in Maryland, New York, Virginia and Washington, the eventual wider rollout of the premium product will help Pepsi boost revenue in its carbonated drinks portfolio, which has been hurt by the commodities businesses of regular and diet colas.

A Few Cases of Craft Sodas

Craft sodas are traditionally made in smaller batches, and feature unique flavor combos like green apple and berry lemonade. "We are finding millennials, in particular, that this authenticity, and its ingredient history, is so important with them, they believe in stories," remarked Lowden. "I think you would be surprised it comes from PepsiCo."

Caleb's Kola will be competing with industry stalwarts Boylan's Soda and offerings from Jones Soda (JSDA). Beverage Digest estimated that craft sodas, although a long-term sales opportunity for PepsiCo and likely Coca-Cola, only have 1 percent share of the roughly 9 billion-case U.S. soda market. The small market share of craft soda highlights the uphill battle for Pepsi's marketing team in trying to get consumers to pay more for a soda that looks the same as others found in glass bottles on retail shelves.

Both Pepsi and Coca-Cola need of whatever innovation -- ingredient or packaging -- their respective R&D teams can cook up to bring sustainable growth back to their U.S. carbonated soft drink portfolios. Overall soda volumes fell an estimated 3 percent in 2013, the ninth straight yearly contraction, according to the latest data from Beverage Digest. Further, estimated U.S. retail sales of carbonated soft drinks declined 1 percent to $76.3 billion, the first downturn in dollar terms in at least 15 years, underscoring the need to boost volumes amid limited pricing power.

In the third quarter, Pepsi's North America non-carbonated beverage volume grew slightly and its carbonated soft drink volume fell 1.5 percent. At Coca-Cola, sparkling and still beverage volume in the Americas each declined 1 percent. Coca-Cola didn't respond to requests for comment.

Getty Images

For all of the things I buy in life, razors seem like the last thing I'd want to buy online. I have a Gillette Mach 3 Turbo razor handle that I bought about 10 years ago, and I buy a 24-pack of razors at Costco (COST) that lasts for a year or more. Yet razors seem to be sold everywhere online.

And online sellers are about $1 cheaper per razor than most stores -- unless you find a heck of a sale (as I did at CVS (CVS)) or you shop at a warehouse store such as Costco. But the catch -- and I'm sure the shaving companies set it up this way -- is that you have to own the correct handle, which can cost up to $25.

Why does a site such as Dollar Shave Club, with its funny videos, or 800razors, with its plain website, or any other online store sell something that's as easy to get as an impulse buy at the supermarket? Two reasons: Razors aren't as inexpensive as they used to be. And they're locked up behind a theft-proof plexiglass case.

Locked Away

At the Safeway (SWY) and CVS stores I went to, razors were in case that a clerk must open. You can't just grab a package and head to the checkout. At Safeway, the Gillette razors were locked in a cabinet, behind a counter, along with cigarettes and the baby formula Similac. Apparently, all of these items were shoplifted so often that stores started keeping them under lock and key.

That's one less incentive to buy them at your local store. Try finding a store clerk on a busy afternoon to unlock a case of razors -- as if you were buying a tablet or e-book reader at Target (TGT) -- so you can shave.

Why Prices Are So High

But the bigger reason for the existence of razors online is the same as it is for most things: a lower price. Procter & Gamble's (PG) Gillette owns 76 percent of the shaving market, and Energizer's (ENR) Schick owns 16 percent, says Phil Masiello, founder and CEO of 800razors.com. With such a stranglehold, those companies can charge a premium. "We got into this because we were outraged at the prices we were paying for razors," Masiello says.

Another way to raise prices is to promote a shaving handle or blade that does things you never thought you needed before. Some have rolling balls or vibrate and are powered by a battery to provide a closer and easier shave.

Big companies also have big advertising budgets, which is something online sellers don't. Lower costs in advertising can result in lower costs for the product. The convenience of buying online is another major selling point for online businesses, says Michael Dubin, co-founder and CEO of Dollar Shave Club.

"The entire men's grooming and skin care market has exploded because American men are paying more attention to how they care for themselves behind the scenes," Dubin wrote in an email interview. "Our unique opportunity exists at the intersection of our ability to provide excellent products that make life better in the bathroom and a technical platform that makes life easier outside it."

Gillette almost has a monopoly in drugstores, for example, so going after its major competitor there didn't make sense. Online is a better place to shop by price.

We Compared Prices So You Don't Have to

To get prices down, competitors sell what are basically knockoffs of popular selling blades. Shaving is subjective, with some preferring five blades to three. For comparison purposes, we tried to find five-blade razors, though some of the most common razors sold in stores have three blades. We priced the most popular razors on the market.

It's also assumed that shoppers already own the handle for the blades they're buying, though the online blades may initially cost more overall because you'll need to buy a handle.

Razors are listed by store or website, razor name and number of blades, and cost per cartridge, going from most expensive to cheapest:

Safeway: Gillette Fusion Proglide, four blades, $4.50 per cartridge.

CVS: Gillette Fusion Proglide, four blades, $4.18.

CVS: Gillette Sensor, three blades, $3.18

Costco: Gillette Fusion Proglide Flexball, four blades, $3.99.

CVS: Schick Hydro 5, five blades, $3.15

Shave MOB, an online store: Caveman razor, six blades, $2.99, including handle.

Shave MOB: Average Joe razor, four blades, $2.74, including handle.

Costco: Schick Hydro 5, five blades, $2.26

Dollar Shave Club: The Executive, six blades, $2.25

800razors: five-blade razor, $2.16. Price rises to $2.49 per cartridge when the $3.99 handle added.

Costco: Gillette Mach 3 Turbo, three blades, $2.08

Harry's, an online store: five or three blades, $1.88, but handle costs $10 to $25, increasing average cost to $3.12 to $5, depending on the one-time handle cost.

CVS: Gillette Fusion Proglide, four blades, $1.66 during a major sale.

Dollar Shave Club: The 4X, four blades, $1.50

The Verdict

Dollar Shave Club beats them all, at least in price. It's a subscription plan, which is easy enough to change if you remember to. Otherwise, your credit card will keep being charged $6 a month or whatever plan you choose.

As one Dollar Shave Club customer told me, the benefit was more than saving money, but in saved time and less hassle. "I would always forget to buy the blades and end up using a dull razor for weeks," says Bill Balderaz, president of Fathom Healthcare, of buying at a store. "I would buy a different handle each time because I would forget if I had the second or third or max or extreme version of the razor at home."

When my Costco supply runs out in a year, I'm going to have to give all of these online stores a try. A low price is good, but if I can find a better shaving experience at a comparable price online, I'll be able to avoid long lines at the store.

NEW YORK -- Leading U.S. CEOs, angered by the Obama administration's challenge to certain "workplace wellness" programs, are threatening to side with anti-Obamacare forces unless the government backs off, according to people familiar with the matter.

Major U.S. corporations have broadly supported President Barack Obama's health care reform despite concerns over several of its elements, largely because it included provisions encouraging the wellness programs.

I don't think the White House would want the CEOs turning on them and supporting these efforts on the Hill.

The programs aim to control health care costs by reducing smoking, obesity, hypertension and other risk factors that can lead to expensive illnesses. A bipartisan provision in the 2010 health care reform law allows employers to reward workers who participate and penalize those who don't.

But recent lawsuits filed by the administration's Equal Employment Opportunity Commission, challenging the programs at Honeywell International (HON) and two smaller companies, have thrown the future of that part of Obamacare into doubt.

The lawsuits infuriated some large employers so much that they are considering aligning themselves with Obama's opponents, according to people familiar with the executives' thinking.

"The fact that the EEOC sued is shocking to our members," said Maria Ghazal, vice-president and counsel at the Business Roundtable, a group of chief executives of more than 200 large U.S. corporations. "They don't understand why a plan in compliance with the [Affordable Care Act] is the target of a lawsuit," she said. "This is a major issue to our members."

"There have been conversations at the most senior levels of the administration about this," she added.

Business Roundtable members are due to meet Obama in a closed-door session Tuesday, where they may air their concerns.

It isn't clear how many members of the group, whose companies sponsor health insurance for 40 million people, are considering any action. It is also not clear if the White House can stop the EEOC from challenging wellness programs.

A threat of a corporate backlash comes at a time when Obama faces criticism even from his Democrats' ranks that he had devoted too much political capital to health care reform.

Such action could take the form of radical changes in health benefits that employers offer. It could also mean supporting a potentially game-changing challenge to Obamacare at the Supreme Court next year and expected Republican efforts to eviscerate the law when they take control of Congress in 2015.

Carrots and Sticks

Obamacare allows financial incentives for workers taking part in workplace wellness programs of up to 50 percent of their monthly premiums, deductibles, and other costs. That translates into hundreds and sometimes thousands of dollars in extra annual costs for those who don't participate.

Typically, participation means filling out detailed health questionnaires, undergoing medical screenings, and in some cases attending weight-loss or smoking-cessation programs.

One of the arguments presented in the lawsuit against three employers is that requiring medical testing violates the Americans with Disabilities Act.

That 1990 law, according to employment-law attorney Joseph Lazzarotti of Jackson Lewis in Morristown, New Jersey, largely prohibits requiring medical tests as part of employment.

"You can't make medical inquiries unless it's consistent with job-necessity, or part of a voluntary wellness program," he said.

The lawsuits are based on the view that it is no longer voluntary if employees face up to $4,000 in penalties for non-participation, loss of insurance or even their jobs.

Employers, however, see the lawsuits as reneging on the administration's commitment to an important part of the health care reform.

On Nov. 14, Roundtable president John Engler sent a letter to the Labor, Treasury and Health and Human Services cabinet secretaries who oversee Obamacare asking them to "thwart all future inappropriate actions against employers who are complying with" the law's wellness rules, and warning of "a chilling effect across the country."

Asked for a response to the letter, an administration official told Reuters that it supported workplace health promotion and prevention "while ensuring that individuals are protected from unfair underwriting practices that could otherwise reduce benefits based on health status."

Undermining Obamacare

In practical terms, large corporations have several ways to undermine Obamacare if they decide to.

One is to support legal challenges to the subsidies given to low-income individuals who buy health insurance on the federal exchange established under the law. Neither the Business Roundtable nor any of its CEO members have done this so far. The Supreme Court is expected to hear oral arguments in the case in 2015.

Another option is to make top executives available for hearings on repealing or diluting Obamacare. "We never did this before," said the person familiar with the executives' thinking. "But they could turn up the noise. I don't think the White House would want the CEOs turning on them and supporting these efforts on the Hill."

The nuclear option would be to radically change employer-sponsored health insurance. Large corporations are highly unlikely to eliminate it, but they might give workers a fixed amount of money to buy coverage on a private insurance exchange. That would allow employers, almost all of which pay workers' medical claims out of their earnings, to cap their health care spending.

For many, Black Friday is a jump start to the holiday shopping season. But if you've never been a fan of crowds, there's a way to get what you need or want without leaving the house. While everyone fights for a parking spot and loses sleep, you can stay in on Black Friday and shop on Cyber Monday instead.

Cyber Monday is the Monday after Thanksgiving and Black Friday, and it's one of the best days to shop online. Several online retailers participate in Cyber Monday by offering online-only sales and promotions, as well as free shipping with no minimum. The deals typically start at midnight Eastern time on Sunday night, reports BuyVia.com. So, if you can stay up a little later, you can snag your deals early and still be on time for work.

But just like Black Friday, you need a strategy for Cyber Monday. However, since many Cyber Monday sales aren't revealed until the weekend before or the actual day of, there isn't a lot of time to plan. You need reinforcement -- a way to find the best deals quick. Fortunately, you can download several apps to your smartphone or tablet to save time and money.

1. Savings.com. Download the Savings.com app for Cyber Monday deals and stay one step ahead of the game. This app is free and easy to use. It's an excellent way to search for the best Cyber Monday online deals, allowing you to purchase what you need before retailers sell out. You'll gain access to the latest coupon codes, plus you can seamlessly compare prices across multiple retail sites in one place. The app has deals from over 25,000 retailers, such as Macy's (M), J.C. Penney (JCP) and Home Depot (HD).

2. BuyVia. Download the BuyVia app and find online-only Cyber Monday deals offered by your favorite retail stores. Search for the lowest prices on items at Amazon.com (AMZN), Macy's, Target (TGT), Walmart (WMT), Best Buy (BBY) and Toys R Us, just to name a few. With the app's customizable features, you can select products you're looking to purchase and then receive an alert when the item goes on sale. If you use deal websites, such as Groupon and Living Social, the app can bring all of your favorite sites together in one place for easy comparison shipping.

3 Coupons at Checkout. Cyber Monday deals and sales are better when paired with a coupon code. And fortunately, several retailers allow customers to combine a coupon code with discount prices. Coupons at Checkout is a free app and one of the fast ways to find coupon codes while you shop. You don't have to comb the Internet or search high and low for a discount code. Simply type the name of the retailer of choice and the app searches for available discount code savings.

4. RetailMeNot. The RetailMeNot app is extremely easy to navigate. Scouring the Internet for the best deals takes time, but this app does the hard work for you. Whether you're looking for the best deal on a tablet computer, household goods or clothing, this app searches for deals and coupons at over 50,000 retailers. All you have to do is enter a retailer's name or a specific item, and RetailMeNot goes to work. It complies a list of coupon codes, best offers and other promotions in just a couple of clicks.

Bonus -- CyberMonday.com. We might be examining the best apps, but CyberMonday.com deserve a mention. To get your online shopping day off to a good start, you need to visit the official Cyber Monday website -- with deals from over 800 participating retailers. You can shop by category, featured deals, or search the site for coupon codes or specific retailers. CyberMonday.com saves time and money; and when you locate a coupon code or deal you like, just click the link and you'll be directed to the retailer's website.

NEW YORK -- For Kathy Murphy, the difference between being gay or straight is $583 a month.

Retirement should have been a "slam dunk," the 62-year-old Texas widow says. She saved, bought a house with her spouse and has a pension through her employer.

But Murphy's retirement hasn't been as secure as it should have been. She is missing out on thousands of dollars a year in Social Security benefits simply because she was married to a woman, not a man.

I never thought I would live to see same-sex marriage, but the government still minimizes my marriage and my relationship of 32 years.

Murphy fell into a loophole in Social Security that denies survivor benefits to same-sex couples depending on what state they live in. Had Murphy and her wife, Sara Barker, lived next door in New Mexico, a state that recognizes same-sex marriage, this wouldn't have been an issue.

"I never thought I would live to see same-sex marriage, but the government still minimizes my marriage and my relationship of 32 years," Murphy says.

Murphy could be thought of as just one of the many baby boomers who aren't prepared for retirement. But while the group overall isn't ready to stop working, gay boomers face challenges that make them even more vulnerable, experts say.

Decades of workplace discrimination impaired their earnings. The AIDS crisis frightened many HIV-positive gay men and women into thinking they wouldn't live long and discouraged them from saving. Legal loopholes within Social Security have left gay boomers with less income.

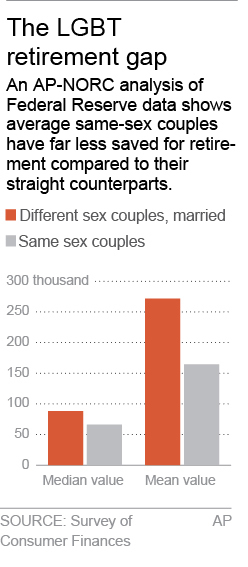

Same-sex couples in general are likely to have saved less for retirement than their straight counterparts, according to an exclusive analysis of the Federal Reserve's Survey of Consumer Finances by the AP-NORC Center for Public Affairs Research. The center is jointly operated by The Associated Press and NORC, a leading research center at the University of Chicago.

The median retirement savings for a same-sex couple is roughly $66,000, while straight married couples have roughly $88,000, according to the data, which looks at the finances of straight and same-sex couples aged 19 to 95 going back to 2001.

"In the aging world, there has been little regard for even the existence of LGBT older people, let alone their particular social and financial needs," says Michael Adams, executive director of SAGE, a national organization focused on social services and advocacy for lesbian, gay, bisexual and transgender seniors.

Lower Earnings

Gays and lesbians have faced higher unemployment, lower wages, and workplace discrimination. While many corporations have non-discrimination policies now, it is still legal to fire someone for their sexual orientation in 27 states, according to the American Civil Liberties Union.

Two studies, one by Pew Research in 2013 and one by Gallup in 2012, concluded that LGBT individuals were more likely to make less money than their straight peers during their careers. A study by the Williams Institute, a California-based think tank, showed gay men earned as much as 32 percent less than straight men.

As a result, gay men and women over 65 are more likely to end up in poverty. The Gallup poll found that 15.9 percent of gay men over 65 were near or below the Federal poverty line, compared to 9.7 percent of heterosexual men in the same age group.

A 2009 report by the Williams Institute showed lesbian couples over the age of 65 were twice as likely to live below the poverty line as opposite-sex couples.

Married Without Benefits

Core elements of the retirement safety net available to married straight couples -- receiving Social Security benefits and pensions -- have not existed for gay Americans.

Heterosexual spouses can typically collect Social Security based on the higher earner's work history. Not so for many gay couples. The federal government did not recognize same-sex marriages at all, even in states where marriage was legal, until last year, when the Supreme Court struck down the Defense of Marriage Act.

"Social Security is the most important financial resource for older Americans in this country, and this is just as true for LGBT older Americans," says SAGE's Adams.

In the case of Murphy and Baker, the couple got married in Massachusetts in 2010. Baker died in 2012 and since then Murphy has been unable to collect her wife's benefit of $583. Same-sex marriage has been legal in Massachusetts since 2003, but it's not allowed in Texas, and the federal government is required by law to use the couples' state of residence to determine benefits.

The Shadow of AIDS

The AIDS epidemic killed nearly half a million Americans before effective medications were developed. It also left a financial scar by discouraging gay men and women from saving.

For some people infected by HIV, a fatalistic attitude took hold, experts say. Why save for the future when the chance of living another five years was slim?

By the time life-prolonging antiretroviral "cocktail" therapies emerged in the late 1990s, HIV-positive baby boomers had lost a decade or more of savings time.

Jim Albaugh is one of those people. Diagnosed with AIDS in 1990, he was in and out of hospitals. After coming back from the brink of death, he now faces another crisis: He has little savings and can't work as much as he did before his illness. Without public financial support programs, he would not be able to get by.

The 53-year-old has 12 years before he hits retirement age, but when asked about it, he says: "I don't think about retirement because I don't believe I will have one."

TIM SLOAN/AFP/Getty ImagesJames M. Simons hired people experienced with science, not finance, to build his company.

Who among us hasn't looked through the annual Forbes 400 list and wondered what it would take to join those financial elites? For James M. Simons, one of the most successful hedge fund managers in history, the path to mega-wealth began in a very ordinary way, as a math professor.

Simons, the son of a shoe factory owner, began his fascination with math at an early age. "I wanted to do math from the time I was 3 years old," says Simons, who was raised in Boston. "Literally, I would think about numbers and spaces."

That fascination led him to attend the Massachusetts Institute of Technology, where age 20 he received a bachelor's of science in math and then three years later a doctorate in the same field from University of California, Berkeley. Under normal circumstances those types of degrees would lead to -- and end with -- a career in academia, something he pursued first as a professor at MIT and then later at Harvard University. But Simons had a restless mind.

Government Cryptology

In 1964, while teaching at Princeton University, the Institute for Defense Analysis -- a covert contractor for the National Security Agency -- recruited him into its cryptology division. For three years he worked on breaking codes and tracking military threats in the escalating Vietnam War, until one day his personal beliefs put him on the wrong side of his employer.

His boss at the institute was Maxwell D. Taylor, a retired four-star general and vocal war hawk. In a 1967 New York Times article, Taylor defended the U.S. involvement in the war, something Simons disagreed with. In a response, also published by the The Times, he spoke out against a continuing military presence in Southeast Asia, encouraging America to pull out "with the greatest possible dispatch."

Summarily let go, Simons soon found himself at a small Long Island college, Stony Brook University, where he headed the math department. He was 30.

A Breakthrough Paper

While at Stony Brook, Simons authored a paper titled "Characteristic Forms and Geometric Invariants" that put his star on the rise in the world of mathematics. The paper changed the way math was thought of and still has applications today in diverse areas, such as quantum physics and string theory.

While at Stony Brook, Simons began to get involved in the stock market, trading in his spare time with the money he had received as wedding gift from his first marriage. Slowly he began to transition from academia to the business world and in 1978 made it official by starting Renaissance Capital with an office in a strip mall.

His first fund -- Limroy -- was based on fundamental research, but Simons found that bored him so he decided to switch to a technical trading approach based on the theories he knew so well from the world of math. In 1988, he launched his Medallion fund, which incorporated futures, interest rates and currency trading.

Lab Work, Not the Trading Floor

Simons continued to build Renaissance -- though not in a traditional way -- in the way he understood best. Job applicants with Wall Street experience were shunned, while those with a scientific backgrounds were hired. Simons staffed his company with hires from the best in physics, computer programming, cryptography and math.

That approach seems to have worked. Renaissance currently manages over $40 billion in assets and has had annual returns that most hedge fund managers would die for -- during the 2008 financial crisis, its Medallion fund was up over 80 percent. And Simons has a reported net worth of $12.5 billion

Simons, who at age 76 is technically retired, still stays involved with the company but more often can be found reading the latest mathematics papers or attending a benefit for one of the many charities he supports. A well-known philanthropist, one of the beneficiaries of his largess was Stony Brook.

In a 2009 Simons gave the university $60 million, commenting, "It's because I'm very fond of Stony Brook. It was my first administrative job. I helped build the university in a modest way. I met my wife there."

Subscribe to my newsletter The Lund Loop a free once-weekly curated slice of what I'm writing, reading and hearing about in the stock market.

wavebreakmedia/Shutterstock

Seventy of incoming college freshman told us that they have never been taught basic financial literacy skills. Yet, they are signing up for student loans, opening credit cards and making decisions that will have a serious impact on the rest of their lives. Why don't we do more to help our children prepare for a financial world that can be extremely expensive when not understood properly?

As a society, we spend a lot of time, money and effort helping prepare our young people for college. SAT preparation is a massive industry. And there are even consultants like Steven Ma, who will charge thousands of dollars to help students gain admission into the best schools.

Yet, for some reason, we do not spend a whole lot of time educating potential college students on the less exciting topic of financial literacy, which is the elephant in the corner.

At MagnifyMoney, we worked with Brooklyn College to design a basic course available to college freshman that focuses on four areas:

The power of compounding interest.

Your credit score and how it is calculated.

How to understand the true cost of banking products and make informed decisions.

The psychology of money and its impact on decision-making.

And at the end of course, we have surveyed our students. Shockingly, but not surprisingly, more than 90 percent wish that they had more financial training earlier in life, preferably in high school. They were already starting to feel the pain of overdrafts and credit card interest, and they didn't like it.

Compounding Interest

Few people understand the true power of compounding interest. We ask the students how long it would take to pay off a $5,000 credit card balance if you only pay the minimum due. Students always underestimate the time (over 20 years) and cost (more than double) that it would take to pay off the balance. I wish I could capture the look on their faces when the true cost is revealed.

But compounding interest does not have to work against you, if you save money. Earning interest on interest by starting to save early can have a huge impact on whether or not you will be able to afford retirement. Few students believe that just $100 a month put into an investment account can generate at least $500,000 in retirement funds.

Credit Score

I meet a lot of people who just recently graduated from college, and they are shocked at their low credit score. Students will often sign up for a college credit card and receive a $500 limit. Not really understanding that bad behavior stays on your permanent record for seven years, they make sloppy payments and have some fun with the card. And then they enter the real world, and they can't believe the impact of their carelessness.

In their mind, it may have only been $100 worth of fun money that they paid a few months late. But entering the workforce with a low credit score can make so much of your life more expensive.

So, we explain the weird world of credit scoring. Whether you love or hate our societal addiction to FICO, the addiction is real. It only seems fair that students should be taught how the system works. They need to know how important on-time payments are to your score. And they need to understand the concept of utilization, which is particularly important when average credit limits are so low.

The True Cost of Banking

This part of the course is my favorite. I ask students how they buy books. All of them talk about comparison-shopping online for the best deals.

I ask how they buy clothes. Again, they are incredibly savvy with comparison shopping online.

And then I ask them how they choose a bank or a credit card. Virtually all of them answer in the same way: they choose their bank because of their parents, or because the branch is close to them.

When I ask them how they might look if they chose their clothes in the same way that they chose their banks, I get a combination of laughter and horror.

Students need to know that banking products should not be treated any differently: Look for the best deal, and don't be afraid to compare, ditch and switch with frequency.

The Psychology of Money

Many people end up in financial difficulty because they can't control their spending. And it is rarely a big purchase. Instead, it was the accumulation of lots of little purchases over the years. Spending an extra $10 to $20 a day can be an extra $20,000 of debt in just a few years.

Not being able to say no is a big part of the issue. And you can start to see the warning signs early in life. Humor always helps and we show a video where Stanford University professor Philip Zimbardo re-enacted the marshmallow experiment.

In those 4-year-old faces, we see the same trade-off that we need to make.

Children are given one marshmallow. Before leaving the room, Zimbardo tells the children that, if they wait to eat, they will be given two marshmallows when he returns. And then we watch -- and laugh -- as we see the children struggle with something that is so fundamental to our decision-making: do I indulge now, or do I wait and have more later? In those 4-year-old faces, we see the same trade-off that we need to make. Do I buy those shoes, or do I save for retirement?

Although we can't take the marshmallow test later in life (most of us become much better at resisting that particular temptation), we can still take Zimbardo's Time Perspective test today. If you are a Present Hedonist, than you are still eating that marshmallow -- and are at risk of debt, delinquency and worse.

This is a fun way to get students to realize that resisting temptation and delaying gratification is ultimately the key to financial success. Although it is not easy, it can be learned. And, although we laugh at a 4-year-old giving into temptation with the marshmallow, it loses its appeal when you are in your 30s and have a family to support.

This Isn't Difficult