For many the holidays have an unpleasant side effect--debt. It's estimated that the average consumer spent $805 on gifts this past holiday season. It was fun passing out presents in December, but in January the credit card bills start rolling in. For others, the start of the new year brings extra motivation to finally tackle their debt. In either case, consumers flock to 0% balance transfer credit cards at the start of every year.

Transferring high interest credit card debt to a 0% card is appealing. The savings in interest can be substantial and it accelerates getting out of debt. It's nice when the entire credit card payment goes to principal, not interest.

Transferring balances to a 0% card is not rocket science. There are, however, some traps to avoid. Further, not all balance transfer cards are created equal. Some are notably better than others. To get the most out of a balance transfer credit card this season, here are 7 tips to keep in mind.

1. Type of Debt: It's most common to transfer high interest credit card debt to a 0% balance transfer offer. In some cases, however, some want to transfer other types of debt, including school loans, car loans, and medical debt. Not all credit cards, however, allow consumers to transfer non-credit card debt. You can find a breakdown of what type of debt can be transferred for the major card issuers in this guide to balance transfer credit cards.

2. Length of 0% Offer: The longest 0% balance transfer offered today is from Citibank and it lasts for 21 months. After that, the rate on any remaining debt is subject to Citi's regular APR. The offer can be found on the Citi Simplicity card. So if you've been looking for a longer 0% offer, you can stop. They don't exist.

3. Balance Transfer Fee: With one exception, every balance transfer card charges a transfer fee. The fee is typically a percentage of the amount transferred. The most common fee is 3%, which results in a $30 fee for every $1,000 transferred. The one exception is the Chase Slate card. For transfers initiated within the first 60 days there is no transfer fee. The 0% introductory APR lasts for 15 months.

4. 0% on Purchases: Don't confuse balance transfers with offers of 0% APR on purchases. Many cards offer both. With 0% on purchases, the card issuer waives interest charges on revolving balances from purchases for a set period of time, often the same length as the balance transfer offer (but not always). If you need to transfer a balance, make sure the 0% offer applies to balance transfers.

5. Credit Score: Most of the top 0% offers require good to excellent credit. As a rule of thumb, a FICO score of at least 700 or higher should be expected, although many factors go into underwriting and lower scores have been approved.

6. Regular APR: Even the longest balance transfer offers eventually expire. When they do, any remaining balance will be subject to the card's regular APR. As a result, it's important to plan now for how you'll handle this debt when the 0% interest is gone.

7. Think Beyond 0%: While paying no interest for an extended period of time is an attractive offer, many balance transfer cards offer significant benefits. For example, the Chase Freedom card offers a $150 bonus if you spend $500 on the card in the first three months. It also offers cash back of up to 5% and comes with no annual fee. Those benefits are in addition to a 0% APR introductory rate on balance transfers and purchases for 15 months.

No interest credit cards can be an excellent tool to help get out of debt. The key is to avoid any new debt after transferring existing balances to no interest cards. Once transferred, work hard to pay off the card by the time the 0% introductory rate expires. Alternatively, you could transfer the debt again to a new balance transfer card until the debt is paid, a strategy I deployed years ago to pay off my credit card debt.

My late grandfather used to say he would retire when he was dead. True to his word he worked until the day he passed away at 84. Like my grandfather before me I have no intention of stopping work and will probably die at my keyboard with emails from editors about missed deadlines piling up.

The fact of the matter is retirement can be a lot more like work than vacation. Many people put a lot of effort into trying not to be bored. Sure sitting on a beautiful beach or fishing or whatever you like doing on vacation is a great while you're on vacation but when it's all you do every day, it can start to get tired.

Vacations are something we look forward to and have a choice about. Retirement has no such choices. One day rolls endlessly, mindlessly into the next. Don't take my word for it. Think about your last great long vacation and how by the end of it you wanted to go back to work, to your life.

The Solution can be as simple as retiring from one job or career and starting a new one. One way to look at it is to think of your work-life before retirement as working for someone else and your work-life after retirement as working for you. Working at something you are passionate about is great way to slow the aging process and stay active. Because you're "retired" you can do it on your own terms.

Retirement Myth 2 - No Money Problems

This retirement myth comes about from the misconception that life magically becomes less expensive when you retire. It doesn't. Food, fuel, clothing all cost as much as before you retired and what you save on commuting you're likely going to want to spend on keeping busy.

Retirement also means increased medical expenses not because retirement is physically taxing or otherwise hazardous to your health but because you are older and body parts start wearing out faster. Older bodies are like classic cars, in order to keep moving down the road they need a little more TLC.

The Solution starts with not counting on social security alone as your primary means of support. The older you are now, the more you should be putting aside for retirement every year. There are two retirement savings traps people fall into. The first is when they are young and believe retirement is too far in the future to concern themselves with right now so they save little to nothing.

The second retirement trap occurs when the kids are grown and finished with school and before retirement when you put off saving for later so you can start treating yourself now. Striking a balance in your 50s between enjoying your relative youth with increasing savings for the not so distant future is the key.

Retirement Myth 3 - Medicare!

This retirement myth is that starting Medicare will cut my health care costs dramatically. While Medicare is a wonderful program, it is not the be all and end all of personal health care coverage. You will need a Medicare supplement policy to help round out your protection and even with a good supplement you will still have out of pocket expenses.

I'm sure there is some direct mathematical corollary between our age in years and the number of prescription drugs we take. Even if there is no such thing as a fixed relationship, the amount and frequency of medications and their associated cost (deductibles and co-pays) does increase with age.

The Solution is to stay active and get plenty of exercise and eat and sleep well. We could all get away with staying out late and neglecting our bodies when we are in our twenties but we don't retire in our twenties. The best way to control increased health care cost is to need less healthcare in the first place. That means taking better care of yourself now and as you get older.

Many of us have heard the phrase, but most of us never think to ask for a price break while shopping.

According to a 2013 Consumer Reports study, only 48% of people even attempt to bargain for a better deal on the products and services they buy every day-even though a whopping 89% of those who said they did haggle were able to nab a discount at least once.

So why are we so hesitant to even ask? For starters, "many people think that negotiation is reserved for the big boardroom-type deals and don't realize how many day-to-day things, such as retail [items], groceries and medical bills, they could negotiate," says Eldonna Lewis Fernandez, a corporate trainer and author of "Think Like a Negotiator: 50 Ways to Create Win-Win Results by Understanding the Pitfalls to Avoid."

"People are either afraid to ask for a better deal or are convinced it can't happen," he says. "They become their own worst enemy if they don't try. You have to have the 'negotiation consciousness': [the willingness] to challenge everything, be assertive and say, 'This is too much,' or 'This is not reasonable,' or 'Can you help me out?' "

Of course, your chances of success will be helped if you know what surprising products or services are actually negotiable. So we rounded up five things you may not have realized you could haggle over, along with some insider tips that could help you move from too-scared-to-ask to negotiating-ninja status.

1. Haggling Hints for ... Appliances and Electronics

Missed the big-box sale on that washer-dryer set, or need a new big-screen TV for the rec room but don't want to pay an arm and a leg? One smart tactic is to ask about floor models, returns and overstocks, says Kyle James, owner and founder of coupon and bargain-hunting site Rather-Be-Shopping.com.

"Store managers typically want them sold immediately so they don't take up valuable real estate," he says. "These items will typically be marked with a special tag. Start the negotiating at 20% off the asking price and be prepared to meet in the middle." While you're at it, it doesn't hurt to ask if they can throw in an extended warranty or delivery for free.

And if you're in the market for more than one big-ticket item, bundling those purchases may help you gain even more leverage.

James discovered the lure of the bundled sale when he was in the market for a new HDTV and DVD player a few years ago. He walked into a major electronics chain and asked the salesperson to knock off $100 if he bought both right then and there.

"He went and asked his manager, and within a minute, he came back and said they could reduce the overall price by $75," James says.

We've all felt the pinch of interest rates, whether on our credit cards, auto loans, mortgages or student debt-but how much leeway do you actually have to negotiate for a lower one?

One of the biggest factors, of course, is your credit rating and history. "If you've made late payments or have a bad credit score, you're more of a credit risk, so the lender may not lower the rate," says Priyanka Prakash, a finance specialist for FitBiz Loans, an online platform that helps business owners find financing. On the flip side, having a high credit score and a positive payment history only works in your favor.

Additionally, the kind of borrowing you're dealing with is important; the more regulated a particular type of loan or line of credit tends to be, the less likely you'll be able to negotiate the interest rate. "Credit card rates are relatively easy to negotiate compared to rates on other [types of] debt," Prakash says. "Student loans are difficult to negotiate because the rates are set at the federal level." Business loans, home loans and auto loans probably fall somewhere in between, she adds.

Showing that you've been shopping around also helps prove how serious you are about finding a lower interest rate. For instance, you could tell your credit card issuer that you're thinking of taking advantage of another company's 0% balance-transfer offer. Or perhaps you have a quote from a lender for a personal loan that you're hoping another bank matches. "Having the quote in writing shows you're serious," Prakash says. Additionally, if there's a timely reason why you're trying to lower your interest rate-maybe a job loss or medical crisis means finances are tight-she recommends having that documentation on hand.

Still unsuccessful? Then try your hand at getting loan fees reduced. Prakash says you'll have more leeway with fees that are charged directly by the lender, such as origination fees, application fees and closing costs, rather than those charged by a third party, such as appraisal fees or credit-report fees.

RELATED: Your Financial Frenemy: Compound Interest

3. Haggling Hints for ... Groceries

Maybe you're already a master coupon clipper-but it's always a win when you can pay even less at checkout, right?

James highlights the deli and meat counters as great places to haggle. "In particular, look for hams and roasts that are less than a pound in size and politely ask for a discount," he says. That's because they may be too small to slice and sell, so the store may be willing to sell them for much less. "Start by asking for 50% off and negotiate from there."

James adds that meats nearing their sell-by date are potentially another good bet, since the store will lose money on them once they expire. "This works best if you're buying more than one cut, so stock up and take it all off their hands for a discount," he says. "Then you can freeze what you can't use in the next day or two."

If your neighborhood has a local farmers' market, you're in luck: They're ripe for heavy discounts if you buy toward the end of the day, says John Vespasian, the author of "The 10 Principles of Rational Living."

"Farmers much prefer to get rid of any remaining vegetables or fruit at a low price, rather than having to haul them back," he says. "This is the perfect opportunity not only to save money by negotiating but also to purchase healthy food."

4. Haggling Hints for ... Moving Services

When you start seeking quotes for movers, the shock can often be enough to make you think twice about relocating. But most people don't realize how much negotiating power they have, regardless of whether they're dealing with big or small moving companies, says Jacob Beckstead, marketing manager at Bailey's Moving & Storage in the Denver area.

Moving companies use different variables to come up with their quotes, but often this is more of an art than a science, says Beckstead. "Moving and storage services can often be negotiated in order to fit your particular budget-especially on such a major purchase," he says. "Even the major carriers with more scientific approaches wouldn't want to lose a sale over 5%."

The services most likely to be negotiable? When a salesperson comes to visit, Beckstead suggests haggling on the packing rates, box rates or hourly loading rates.

5. Haggling Hints for ... Medical Costs

You've gotten over an ailment, and just as you're feeling better, you get your doctor's bill-and it nearly sends you back to the emergency room. Often, consumers feel obligated to pay the bill as is, without realizing that the cost for many types of medical services or procedures isn't set in stone.

First, check that bill carefully-were you billed twice for the same procedure? Were your medical services improperly coded? Ferreting out billing errors could help lower your bill quickly. But if you're sure there are no mistakes, asking your doctor or hospital nicely for a discount could go a long way.

There are a "certain number of patients who never pay their bill, so they'd rather get something than nothing," Brodow says. When he was recently billed $1,800 for a minor lab test, he explained that his insurance wouldn't cover it and that he was older and semi-retired, and then asked if they could adjust the cost. Sure enough, he was able to lower it to $500.

Fernandez says that the billing department can be your ally since they routinely deal with hostile customers. "You will stand out if you leave emotion out and you are kind and cooperative," she says. Fernandez also suggests starting your request with, "Is there any reason you can't ... ?" For example: "Is there any reason you can't delay sending this to collections for a month so I can work on getting it paid?"

"You're not asking, 'Why can't you?' or 'Will you?' You're changing the language of the question to invoke a positive response," Fernandez says. The billing specialists likely won't have a good reason why they can't help fulfill your request. "That interruption [from a typical 'no' response] may be just enough to get the person on the other end to feel a little of the human element, versus the mentality of you just being another cog in the wheel of their job."

They might be better educated and more technologically savvy than previous generations, but that doesn't mean millennials are making smart financial decisions.

Millennials are heavy users of the alternative financial system - which includes payday loans, pawnshops and tax refund advances - and reluctant to seek professional financial help.

That's according to a recent report from tax and consulting firm PricewaterhouseCoopers and the George Washington University's Global Financial Literacy Excellence Center. The report is based on survey results of more than 5,500 millennials (ages 23 to 35).

"Millennials owe a lot. They know too little," said Annamaria Lusardi, academic director at the George Washington University center.

When compared with other Americans, the millennial generation - those born between the early 1980s and mid-1990s - has the "lowest level of financial literacy," the report said. Unfortunately, despite a lack of financial know-how, a mere 27 percent of millennials seek help from a financial professional.

A lack of financial literacy may explain why 42 percent of millennials took out a payday loan or auto title loan, used a pawnshop, got a tax refund advance or purchased a rent-to-own product in the past five years.

"There's an appetite for faster money quicker without thinking of the longer-term ramifications," Shannon Schuyler, head of corporate responsibility and chief purpose officer at PwC, told Moneywatch. "They don't want to ask for help, they are embarrassed, they feel they are in this by themselves, and they are using interesting ways, like taking cash advances on their credit cards" to try to deal with their plight, she added.

Lack financial know-how: Only 24 percent of millennials demonstrate basic financial knowledge and just 8 percent show high financial literacy.

Discontent over financial situation: Thirty-four percent of millennials report being "very unsatisfied" with their current financial situation.

Fret over student loans: More than half of millennials (54 percent) said they're worried about their ability to pay back their student loans.

Financially fragile: Nearly 1 in 3 millennials (30 percent) are overdrawing their checking accounts. (Read more about millennials' financial habits at "Millennials Have No Savings; Here's Why")

Retirement account woes: Just 36 percent of millennials have a retirement account. Of those, 17 percent took a loan and 14 percent took a hardship withdrawal from those accounts in the past year. "This trend is especially worrying because it can compromise millennials' future financial security," the report said.

When you think about doing something, you're obviously more likely to do it. Additionally, what you think about your life, your friends, your family, and your circumstances has a tremendous impact on your financial success.

What you tell yourself matters. Believe me, I know.

When I came back from serving overseas, things weren't easy. I was telling myself things that I shouldn't have been telling myself. These thoughts weighed on me, and they could have affected my financial success.

Thankfully, I soon learned the power of stepping back and looking at the thoughts that were running through my mind. Doing this allowed me to critically examine my thoughts, and replace them with better ones.

I'm sure you understand what I'm talking about. If not, you're probably not human - no offense.

Today I'd like to share with you a few daily thoughts that can help you boost your financial success. Write them down on sticky notes and attach them to your computer monitor, your refrigerator, or anywhere else you visit frequently.

Ready for a mental boost? Let's do this.

1. "My financial situation can change for the better."

If you're under the weight of crushing debt, have just gone through a nasty divorce in which you owe alimony, or lost your house to a fire without the support of insurance, it can be difficult to see a light at the end of the tunnel.

But remember, just because your financial situation looks bleak, that doesn't mean it will always look like armageddon. Time and effort can change things.

If you sincerely believe that you'll always be in debt, you'll always never be able to afford the alimony, or you'll always be renting and never own a house again, you'll probably always be right.

Think about it. If you don't believe your financial situation can change for the better, why would you take the steps necessary to change your financial situation? Boom. Mind blown.

Remember: If you feel fate will keep you muddy in the ditch, then muddy in the ditch you will remain.

Your financial situation can change for the better. You have to believe you can make a change in your life. If you struggle with the idea of making a change for yourself, grab onto the fact that your family and friends need your support. They are counting on you.

Join the Money Uprising Movement[TM] and find hope. It's all about believing you can improve your financial situation and taking action. You can do this.

2. "I can have little and still be content."

Materialism is spreading through our country like a virus. America, I feel, is thoroughly infected by it.

When will we ever learn to be content with our belongings? If you have just one flat screen television, that makes you a rich person, my friend.

But what if you don't even have that? What if you have a few books on the shelf, clothes on your back, and a roof over your head? I'd argue you can still learn to be content. And if you do learn the art of contentment, you'll find that all that extra stuff you've been wanting really doesn't matter much anyway.

By saving money through contentment, you'll be able to boost your financial situation in ways you never thought possible. You'll be able to put more money into retirement savings, help your children attend college, or give to a good cause.

3. "It's okay to take reasonable risks."

A long time ago I knew a woman who decided to take what her mother considered to be an unreasonable risk. Helen took out a personal loan to launch a brand new business.

She was making a decent living selling cosmetics, so her mother just couldn't understand why she'd take such a risk when she could have just kept on selling cosmetics to make a stable income.

I can understand her mother's concerns. But you know what? Helen's mother isn't Helen. Helen is Helen. Helen knows herself and her intentions better than her mother. And you know what? Helen was right.

Today, Helen has made millions with her business - and it all started because Helen took a reasonable risk, not a foolish one.

Granted, sometimes it is difficult for us to determine what's a reasonable risk and what's an unreasonable risk. Sometimes, it's best to get the advice of our friends and family. However, it might be better for us to get the advice of an unbiased third party - like a financial advisor. Generally speaking, a reasonable risk is one that won't bankrupt us if our idea falls apart. Risk a fraction of your finances, not the whole of them.

If you're not used to taking risks, it's going to be scary when you first try. Overcome your fears and push the boundaries of what you thought possible. It's a good daily thought that can boost your financial success. In fact, it's one of the ways you can think like a millionaire.

4. "I can learn new skills through discipline."

No doubt, you've heard of a stay-at-home mom going back to college to earn her degree. Perhaps you've heard of a man who changed his career as he was nearing retirement age. Maybe you know of someone who read books for hours and learned how to start a new online business.

You know what all of these people have in common? They believed they could learn new skills through discipline. The key word here is discipline.

In order to learn new skills, you have to dedicate yourself to learning them and fight hard to lock them into memory. It's no easy task, and that's why so few people try to learn new skills - especially if they have something already that's "working" for them.

Now, you don't have to dive head first into BASE jumping - that's just plain stupid. Take time to learn. Take the steps necessary. Ease into it. And perhaps try something new other than BASE jumping - for me.

New skills often translate into more money-making opportunities. This, my friend, boosts your financial success. Go learn something new!

5. "If someone's holding me back it's likely to be myself."

It's easy to blame our lack of financial success on others or our circumstances. Here are some common excuses:

"I didn't go to college and can't afford it - I'll never amount to anything."

"The man is holding me down. I just can't beat the system, bro."

"Government is a business killer. Who can afford the taxes?"

While life's circumstances do present obstacles, they can typically be overcome. If that's the case, then what's really holding you back from financial success? Dare I say it's you?

When you dwell on all the reasons your goals are difficult, you're disabling yourself from taking action. It's like the elephant who has had a chain on his leg for years. While he couldn't move with the chain, eventually it was replaced with a string. The string was easily breakable, but the elephant didn't have the insight to see that now was his opportunity to escape his captivity. He thought the string was as strong as the chain - and he was wrong.

How about you? Are you looking to escape your circumstances? Are you sure that the things that held you back in the past are holding you back now? Are you certain that you were ever held back by anything other than your own negative thinking?

If you're starting to see that the wall you're trying to break through is the one you've built, don't worry, you're not alone. Countless people build their own walls and blame the brick-maker.

My goal is to show you that you don't have to hold yourself back. The future is a blank slate. You just have to write the story.

I challenge you to keep these thoughts in your mind as you go throughout your day. Don't forget them. Do what I said and write them down. Meditate on them. Your thoughts have a tremendous impact on the degree of your financial success. Train yourself to think positively and transform your mind. You'll be better off for it.

Critics of American work culture have long complained that the 9 to 5 is no way to be alive. This lifestyle model was most culturally visible in the 50's, when men with hats and briefcases became iconic symbols of hard work, the virtue which fueled family, freedom, and the American Dream! These values made war with America's burgeoning Counter-Culture over the coming decades, and the cultural pendulum, for many, swung away from hard work as an ethos to be respected.

Today, the pendulum seems to be hanging somewhere between these two extremes. Even as we hear of reports of all-or-nothing work requirements at places like Amazon, many Americans want a more humane way to make a living. This is what we mean when we talk about a Work-Life Balance. It's a way to make real money, without having to sacrifice health and happiness to do so. It's a way to be able to raise a family, without having to be destitute. It's a way to prepare for retirement, without giving into some of the nastier aspects of 21st century capitalism. Basically, it's the new American Dream, and people want to achieve it.

Various studies paint the Millennial generation as a group of people who want to find fulfillment, at least in part, outside of the workplace. Nonetheless, Millennials tend to be freaked out about money. You know all about the challenges that today's 20- and 30-somethings endured as they entered adulthood. Work hasn't been the bedrock institution that it was for some previous generations. Despite being difficult to corral into cubicles, Millennials tend to hope for financial security, and even independence. Is it possible to achieve one or both of these goals, all while maintaining a healthy life of experience outside of a normal job?

Cracking the Work-Life Balance Code: Real Life Methods

A healthy work-life balance is by no means limited to the young, but it's easier to lay the foundation for this lifestyle if you have personal freedom and plenty of years to implement your strategy. Still, many of the following methods are available to all.

1. Move. Millennials are a mobile generation. One of the biggest factors is cost of living. The past couple of decades may have been hard for American cities like Buffalo, Baltimore, and Detroit, but this has only made them very attractive for young people, for whom homeownership, startup jobs, and entrepreneurial efforts would be more inaccessible in thriving cities. If you want the money you make to go farther, or to be able to work less to make ends meet, why not move to a place where it doesn't cost so much to do what you do? This goal even leads some people out of the country on a permanent or semi-permanent basis.

2. Educate Yourself. Unless you have marketable skills, it may be hard for you to make money very quickly. We're not talking 6 figure earnings, here. But unless you're able to earn enough to support a simple lifestyle without working 60 hours a week, this whole work-life thing isn't going to happen for you. This knowledge has led thousands of Americans into growing sectors like nursing, and this option (with its 4-day workweeks and job mobility) may be an option for you.

3. Practice a Well Rounded Lifestyle. Even if you haven't "arrived" yet, start making time for meaningful life outside of the workplace, even if that's challenging. Some people recommend the Hobby Approach, where people cultivate three main hobbies in their lives: one to stay fit, one to make money, and one to exercise their creativity. By living a meaningful life, even when it's easier to punch the clock until you come home and fall asleep to Netflix, are essential to building a life that's enjoyable within and without the workplace.

4. Save and Invest. Live beneath your means and save/invest for the future. You don't have to be a professional investor or a high earner to do these well. But without them, even the best-lived life will be difficult to sustain as the years go by.

5. Have Relationships. Many people enter adulthood only to realize they no longer have any friends. Don't let this happen to you. Make time for relationships, for your family, for your kids. Go out for drinks, go for a hike, get together even if you're tired. Without meaningful relationships, none of the rest of this will do much to scratch the work-life balance itch.

You'll have to pioneer your own methods to make this work for you. Everyone is different, and will have different expectations for what a good work-life balance is. Making this happen is hard work, but don't stop. It's possible to be happy and fulfilled, even if you have to work for money.

Winter is here, and that cold weather can affect your home and your savings. Luckily, there are a few things that can help you make it through the season and save a few bucks, too.

First, you shouldn't have to blow through your savings to stop cold drafts from blowing through your house. Many retailers sell draft blockers for $15, but at your local hardware store you can get the same result for a tenth of the price with a roll of pipe insulation. Simply measure and cut a piece to fit your door. Then just slide the foam in and you're done.

As for those drafty windows, a window insulation kit should do the trick -- plus, they're easy to install. Just line your window frame with the double stick tape, put on the plastic covering and then trim the excess to fit the window.

You can also use a blow dryer to eliminate wrinkles in the film, making it nearly invisible. These kits cost about $5 (to cover two windows) and can save you up to $17 per window on your energy bills this season. How's that for winter savings?

Finally, your house isn't the only thing susceptible to the elements. When it comes to your car, a foggy windshield can be a real pain. Store-bought defogger spray can cost you up to $7 per bottle, but it turns out shaving cream works just as well. Simply spread a thin coat onto the inside of your windshield, and wipe it down with a clean cloth. This will keep your windshield clear and shave a few dollars off your winter spending.

This winter, don't let a cold home freeze over your savings. Give these tips a try, so you and y our budget stay warm this season.

One could argue that 2015 was the year of the $15 minimum hourly wage. But 2016 could provide another big boost to efforts to hike pay.

Fourteen cities, counties and states approved $15 minimum wage laws this year, according to newly released data from the National Employment Law Project (NELP), a nonprofit that advocates for low-wage workers.

Christine Owens, executive director of NELP, says in a recent news release that the past year has seen "incredible momentum" to raise wages. The press release adds that 2016 shows more promise:

The Fight for $15 is expected to make further inroads in the New Year. There are 16 pending legislative or ballot proposals in 15 jurisdictions that will likely gain traction in 2016.

The New York City-based nonprofit notes that action on federal legislation - which would more than double the current federal minimum wage of $7.25 - is "unlikely in the current Congress." Details on the pending initiatives are as follows:

Federal: Proposal for a $15 minimum wage that would be phased in by 2020

New York: $15 by 2018 (for New York City) or 2021 (for New York state)

California: $15 in two proposals - one by 2021; another by 2020 for businesses with 25-plus workers, 2021 for businesses with fewer workers

Washington, D.C.: $15 by 2020

Massachusetts (fast food and big retail): $15 by 2018

Oregon: $15 by 2019

Missouri: $15 by 2023

Olympia, Washington: $15 (no date given)

Sacramento, California: $15 by 2020

Pasadena, California: $15 (no date given)

Palo Alto, California: $15 by 2018

Sunnyvale, California: $15 by 2018

Berkeley, California: $15 by 2018 for businesses with at least 55 workers; or 2020 for businesses with fewer than 55 workers

Investing and planning for the future can be a daunting task. There are so many factors to consider in creating and managing your portfolio, and you may find it difficult to find a financial professional you trust for unbiased advice.

That's why Monument Wealth Management, as an independent registered investment advisor, has prepared this list of seven considerations to help prepare you to make investment decisions and facilitate a conversation with a financial advisor.

What's your goal? There are lots of reasons to sock money away for growth: emergencies, home down payment, education and retirement are only a few examples. Understanding your liquidity needs and investing goals help you decide which investments will provide the funds you need at the right time.

What do your finances look like right now? Do you have three to six months in savings for living expenses? How much debt can you eliminate? Prioritize what you are saving for according to your current financial situation. You want to be able to invest consistently over time, even if the amount is small, but without putting yourself at risk of not having cash when you need it or having to liquidate investments early. Managing your household's cash flow is key.

When do you need money? Some investments are more easily liquidated than others. There are tax implications whenever you sell an asset. High-risk assets are more appropriate for longer time frames. Plan for your cash needs 12 to 18 months in advance so you will be able to make thoughtful, rather than emotional, decisions for any changes to your investment strategy. Market fluctuations are the primary reason investors make bad decisions. Eliminate this by predetermining your liquidity needs.

How do you feel about risk? Every investment decision has an upside and a downside. How certain and how large does the upside have to be to make you comfortable with the downside? Not only does risk tolerance vary for each person, it can vary for the same person over time depending on age, changes in life circumstances, what is happening in the market or in other news. Assess your comfort with risk periodically. We have a unique way to determine your risk by answering questions about your behavior.

Is your investment portfolio diversified? Investing 101 says not to put all your eggs in one basket. But what does that really mean? There are lots of ways to diversify - by investing in different companies, industry sectors, geographical markets, asset classes (because having all your money in stocks isn't really a diverse portfolio), and different investment time frames. Diversification on many levels provides some insulation from market fluctuations, because what is bad for some markets is good for others, and short-term investments provide opportunities to rebalance. Diversification is much like the pistons of an engine moving up and down, driving a car forward. The more pistons in the engine, the more powerful and smooth the car runs.

How involved do you want to be in managing your investments? You can be super-involved, daily if you want; there are many tools and resources available for active and sophisticated investors. We don't recommend this approach because it is risky and too easy to make emotional decisions that compromise long-term performance. Many people do not have the time or inclination to be quite so involved and may choose more traditional investments or delegate portfolio management to a financial advisor. There are many ways to invest and levels of involvement, but the most important factor is to make sure your investments are in sync with your long-term financial plan.

There is only one sure thing. The market is going to go up! Then it's going to go down. Then it's going to go up! Then down ... up ... down ... and so on. Knowing this, keep your eyes on your plan rather than "panic selling" your assets. It is easy to see the market dropping and want to jump out of your investments; as long as you have a long-term plan, investments aligned with that plan and enough cash set aside for emergencies, you should be just fine even in a market downturn.

Our advice to you is to know your goals, know yourself and have a plan. We would be happy to help with any of your investment planning questions and help you develop a plan to meet your life goals.

When you hear the words "retirement destination," places in Arizona and Florida probably spring to mind. But broaden your horizons, and you can find plenty of other great options all across the country.

The following 15 spots may not be popular with retirees now-but contrarian living comes with benefits. Some of these places may offer tax breaks or other perks to try and lure in more older residents. Plus, the existing younger crowds might help keep you young and active.

Check out our list of surprising places for retirement that you probably haven't considered, and see if any hold appeal for your own new home:

Chick-fil-A is among the most successful fast-food chains in the US, and it's also one of the cheapest to open.

The company grew by $700 million to achieve $5.8 billion in sales in 2014, making it larger than every pizza brand in the country, according to QSR magazine.

Chick-fil-A is now the eighth-largest fast-food chain in the US by sales, and it generates more revenue per restaurant than any other chain nationally, according to QSR.

Despite its success, Chick-fil-A charges franchisees only $10,000 to open a new restaurant, and it doesn't require candidates meet a threshold for net worth or liquid assets, the company told Business Insider.

That's cheaper than every major fast-food chain in the US.

McDonald's, for example, requires potential franchisees to pay between $955,708 and $2.3 million in startup costs - including a $45,000 franchise fee - as well as have liquid assets of at least $750,000.

Taco Bell's startup costs average $1.2 million to $2.5 million and the company requires a minimum net worth of $1.5 million and liquid assets of at least $750,000.

Chick-fil-A, on the other hand, pays for all startup costs - including real estate, restaurant construction, and equipment.

In turn, the company leases everything to its franchisees for an ongoing fee equal to 15% of sales plus 50% of pretax profit remaining, Chick-fil-A spokeswoman Amanda Hannah told Business Insider.

"The barrier to entry for being a franchisee is never going to be money," Hannah said. "We seek to find the very best business partners who find great joy in making other people's days. They do so with a combination of great business acumen, an entrepreneurial spirit, and a passion for serving others."

So what's the catch?

While Chick-fil-A's startup costs are low, the ongoing fees are higher than those charged by many of its rivals.

McDonald's, for example, charges an ongoing monthly service fee equal to 4% of gross sales and an additional fee for rent, which is also a percentage of sales. McDonald's franchisees have historically paid about 8.5% of sales in rent costs, though some pay as much as 12%, according to a 2013 Bloomberg report.

Chick-fil-A also prohibits most of its franchisees from opening multiple units, which can limit franchisees' potential profits.

This limitation is meant to enable Chick-fil-A's franchisees to be intimately involved in the day-to-day operations of their restaurants.

"Chick-fil-A operators must be as comfortable rolling up their sleeves in the kitchen as they are shaking hands in the dining room," Hannah said.

The company also puts a big emphasis on community service and encourages franchisees to be actively involved in the communities where they live and work.

"Oftentimes, several operators in a market will combine resources to market events through advertising and promotion," Hannah said. "Our daddy-daughter date nights are an example of this."

The application process

Chick-fil-A gets more than 20,000 inquiries from franchisee candidates every year. From those candidates, Chick-fil-A selects between 75 to 80 new franchisees annually, Hannah said.

Chick-fil-A will then contact the candidates for interviews. The company may also interview candidates' friends, family members, and business partners.

Once they are selected and hired, franchisees have to undergo a multi-week training program before they can open and operate their own restaurant.

Car salespeople aren't necessarily evil, but they're the only people who can prevent you from getting the best price for your next car. It's a good idea to keep these four car dealer traps in mind the next time you decide to go car shopping. Doing so might save you the gut-wrenching regret of being screwed over and forced to overpay for your new vehicle.

When the salesperson starts talking about monthly payments, watch out.

Clever salespeople want you to focus only on low monthly payments because it gives them room to inflate other variables, such as the loan interest and length. This increases the dealer's profit - while you spend thousands more on the car overall.

Some dealers pull out what's called a four-square chart, which is confusing as hell. A former car salesman unveiled on The Consumerist how that shell game is played: You're put on the defensive and worn down with tricky math, while the salesperson appears to knock down prices.

Counter Strategy: Don't even discuss monthly payments. Tell the salesperson you can talk financing later, but first want to know their best price.

Pay for the car in cash or get your own financing if you can, but don't reveal how you're going to pay until after you've negotiated down the total car price. (Dealers may be less likely to negotiate if they know they can't profit from your financing.)

If you do need to discuss dealer financing, do that after you've negotiated the car price. From there you can focus on the annual percentage rate (APR) rather than payments.

Dealer Trick #2: Telling You Your Credit Sucks

If you don't know your credit score, all dealerships have to do to rip you off is say you don't qualify for a better rate. Perhaps a bank would offer a 5% loan; the dealer might say 7% is the lowest for your credit score.

Counter Strategy: Pull your credit report for free and know your credit score before setting foot in a dealership. Again, shop around for financing and get it on your own if you can. Whatever your credit score, at least you'll know if the dealer's trying to pull a fast one on you.

Salespeople can disarm you with humor and appear to be on your side in your battle against a faceless manager in the back room. You might even get a great trade-in offer or discount on the total price.

Inevitably, lowball offers and inflated trade-in values are squashed by the manager later. Edmund.com's Confessions of a Car Salesman series reveals how numbers previously agreed upon can somehow be "lost" or "forgotten" by the dealership.

Counter Strategy: Not all car salespeople are scumbags, but remember, they're doing their jobs and are not your friends. Don't fall for the good guy/bad guy game, and walk if they don't honor what you agreed upon. Better yet - get a copy of the numbers in writing from the dealership.

Dealer Trick #4: Pushing Add-Ons and Fees

Finally, be on the lookout for extras added to your purchase or financing. Dealers can increase your car payment price by "packing" extras like an extended warranty, perhaps saying it's "only $40 more" a month. That $40 extra will cost you $2,400 over a 60-month loan.

Counter Strategy: Know which add-ons are truly unnecessary and check the financing and sell sheets carefully. Things you shouldn't be charged for include a hidden loan acquisition fee and other fees, such as "customer service" or doc preparation fees.

You only need to do two things to come out on top: research car prices and comparison-shop multiple dealerships. One recent car survey found that knowing the dealer's invoice prices and visiting two dealerships saved car buyers an average of $800. TrueCar, Kelley Blue Book and Edmunds.com can all help you find invoice prices and what your trade-in is worth.

My favorite method is simply this one published on GetRichSlowly.com: email all of the dealers near you and say, "Hi, my name is so and so. I plan to buy such and such a car today at 5pm. I'm going to buy it from the dealer who gives me the best price. What is your best price?" Bam. Straight to the chase.

People move for many different reasons. For instance, some get new jobs, others retire, and some just want to be closer to their families.

While many people in the US move within the same state - the Census Bureau estimated in 2011 that 40% of moves are within 50 miles - there are patterns for those who did make interstate moves, according to Atlas Van Lines, a national moving company.

Atlas looked at 77,705 interstate moves and found that 18 states had more people moving out than in, whereas 12 had the reverse happen. We rounded up the 18 that had outflows for 2015. Most are in the upper-Midwest, which Atlas said has been on an outbound trend for a while.

"The Midwestern states experienced a major shift to outbound moves, with Wisconsin, Iowa and South Dakota going from balanced to outbound in 2015," said the report. "Similar to 2013 and 2014, North Dakota was the only state in the region to register as inbound."

See the states that topped the list, in order from lowest to higher percentage outbound migration:

National banks are still struggling to shed their collective image as fee-heavy, profit-hungry machines. Despite this reputation, however, national brick-and-mortar banks offer numerous products and services that consumers are still happy to use.

Ubiquitous branches and ATMs, interest-bearing accounts and state-of-the-art technology make the larger, commercial bank the right fit for consumers who need their bank to be everywhere - and who need digital banking services or a wide range of insurance and loan options that many smaller, community financial institutions don't offer.

With so many product and service factors to consider, choosing the right bank with the right blend of amenities to fulfill your needs can be a challenge. Moreover, you want to make sure you're choosing a bank that offers competitive interest rates.

Personal finance website GOBankingRates.com conducted its annual Best Banks study to help you narrow your search. The study assessed the top 90 financial institutions based on asset size according to the FDIC. Check out the top 10 banks to see what they have to offer.

Best Bank: Wells Fargo

Although it doesn't have the highest number of ATMs, Wells Fargo does have the most U.S. branches of any national brick-and-mortar bank on this list - 6,200. It also has other advantages that make it the best bank of 2016. Wells Fargo's array of deposit products, loan and investment service options, and smartphone banking capabilities are hard to match, and it has a BauerFinancial rating of four.

Bank of America

Although its $12 checking account fee is one of the highest on this top 10 list, Bank of America offers a high level of convenience. With more than 16,100 ATMs scattered across the country, customers have the accessibility they need to deposit or withdraw on the go.

Chase

Like Bank of America, Chase's $12 checking account fee is high compared with other banks on this list, but the bank offers a broad range of products that result in convenient banking options. Accessibility through its 5,300 branches and 15,500 ATMs is a major feature for Chase because, although its savings rate of 0.01 percent APY is similar to many banks on this list, its 0.02 percent APY CD rate is one of the lowest on this list.

Citibank

Citibank offers customers a thorough product list, including several credit card choices, from secured and student cards, to rewards, business and travel credit cards. It also offers several investment options for wealth building. It has one of the highest checking fees on this list ($12) but also one of the highest CD rates (0.15 percent APY).

First Midwest Bank

First Midwest Bank is the other financial institution on this list with no checking account fee. Although its branch locations are limited to Illinois, Indiana and Iowa, the bank offers access to more than 50,000 ATMs nationwide through its Allpoint network.

First Niagara Bank

First Niagara Bank offers the highest 12-month CD rate of the Best Banks of 2016: 0.50 percent APY on a $500 minimum opening balance. It also offers the highest savings account rate of any bank on this list at 0.10 percent APY. The bank has nearly 400 branches across Connecticut, Massachusetts, New York and Pennsylvania.

Great Western Bank

Great Western Bank is one of only two financial institutions in this top 10 with no checking fee. It also boasts a 0.15 percent APY CD; a full range of deposit account products as well as loan, investment and insurance services; and a BauerFinancial rating of five. However, its 158 branches are located in the West and Midwest only.

HSBC Bank

If a basic, no-frills checking account is what you want, HSBC is a top choice. Its Basic Banking account carries a fee of just $3. Consumers looking for more features might want to opt for the bank's Choice, Advance or Premier Checking products, which offer additional credit card and relationship savings account options.

PNC Bank

PNC Bank offers a full range of banking and finance products and services, including brokerage accounts, stocks and bonds, education accounts and insurance. It also has the second-highest savings account rate on this list - 0.05 percent APY - if you have a PNC checking account. The checking account has a $7 monthly fee.

U.S. Bank

U.S. Bank has a higher-than-average 12-month CD rate (0.10 percent APY) and a slightly lower checking fee ($6.95) than many of its competitors. It also offers a range of deposit services, credit cards and mortgage and auto loans.

All the top 10 banks of 2016 received a BauerFinancial rating of at least 4 out of 5. Although their deposit account rates are about average, or in some cases lower, compared with what some smaller financial institutions and online-only banks can offer, these national brick-and-mortar banks offer a significant range of banking products, digital money management capabilities, widespread branch and ATM access, and loans and investing services that smaller and online institutions cannot.

Methodology: Rankings were based on criteria such as deposit account interest rates for checking, savings and 12-month certificate of deposit accounts; diversity of products offered, such as auto loans, mortgages, credit cards and investment services; the banks' accessibility in terms of branch and ATM locations; and their BauerFinancial star ratings.

Millennials have had a rough road when it comes to money. Not only did they come of age during the Great Recession, which made jobs scarce and benefits even scarcer, but many saw their parents lose big time in the stock or real estate markets, which scared them off of making their own investments. Still, there's no more time for excuses, because millennials are all grown up and taking on increasing amounts of responsibility. From mortgages and parenthood to caring for aging parents, millennials are facing big financial milestones, whether they're ready or not.

According to Bank of America's Year-End Millennial Snapshot, which analyzed 2015 data from over 3,500 millennials, this young cohort of 20- and early 30-somethings continues to struggle financially: a tough job market, hesitancy to invest and student loans are just a few of the challenges in their way to prosperity. Still, the data suggest they are firmly committed to achieving financial independence one day. About half of millennials said the Great Recession changed the way they think about saving, investing and spending, with 40 percent saying they are more reluctant to invest in the stock market and 36 percent saying they are more hesitant to buy a house.

Yet over 80 percent of millennials are optimistic that they will be able to save and invest more in the future. "There is still a sense of optimism with the millennials. Although they're more hesitant, it's not stopping them. They feel good about the future," says John Jordan, client experience and programs executive for preferred and small business banking at Bank of America.

Many are also getting some big financial assists from their parents, and 46 percent of millennial-supporting parents say they don't plan to stop anytime soon.

A survey by the investment app Acorns of 1,020 millennials found that almost half of those surveyed said they were "treading water" financially or worse and would be in big trouble if they missed a paycheck. Most millennials (85 percent) said they haven't yet invested any money in the stock market, largely because they don't feel comfortable with it. While respondents said they wanted to save more, they found it difficult to do so given the pressures of living expenses and student loans.

"So many millennials are working on a contract basis or as freelancers; they don't have full-time benefits," says Jennifer Barrett, vice president of editorial and founding editor of Grow, a digital magazine published by Acorns and aimed at millennials. "They have to be more proactive ... [and] engage with finances much earlier than with earlier generations. Millennials are on their own in a lot of ways," she says.

That's why forming good money habits is a key part of creating financial stability for the millennial generation, Barrett adds. "We recommend that people get in the habit of investing early on," she says.

That's a message echoed by other millennial financial experts. "The biggest money mistake most people make - and I know I certainly did - is simply waiting too long to care," says David Weliver, 34, founder of the millennial finance website Money Under 30. When you're juggling your career, love life and other big issues, it's hard to also find time for your finances.

After college, young people tend to get bombarded with credit card offers, Barrett says, but they're usually better off skipping them. If you take on credit card debt, especially on top of student loan debt, then it's easy to get stuck in a trap of constantly feeling like you're falling behind. "Some millennials are embarrassed by [their debt]; it weighs pretty heavily on them," she adds.

2. Increase your savings whenever you get a raise.

Anytime you experience a windfall - perhaps you earned a bonus or got a raise - Barrett suggests putting it directly into your retirement savings. "If you can increase your contribution right away before you have time to even register that you have a raise, that's what really makes the difference," she says.

3. Get comfortable with investing.

Because so many millennials are scared of investing in the stock market (and understandably, since they came of age during the Great Recession), Barrett says it's particularly important to dive in early so long-term savings can outpace inflation. At the same time, though, she adds that it's important to have an emergency fund stashed in a safe spot, like a bank account, so you can cover unexpected expenses without reaching for a credit card.

4. "Stop the bleeding."

That graphic expression is how Weliver describes the need to prioritize. "Make sure you're not going into more debt," he says, adding that you should look for ways to downsize your lifestyle or earn more money (or both). Once you find a way to end the month positive at least a couple hundred dollars, then you can start making choices about saving, investing and paying off debt.

5. Pay off student debt.

Student loans are the albatross that hounds so many millennials; Weliver still remembers the day he made his final payment. Along with the day he realized he had enough in savings to live on for a year if necessary, it was a momentous occasion, and one that reinforced his choice to be more conscious about his spending and money management.

6. Imagine your future.

Considering where you want to be down the road can help you make the right choices today, Weliver adds. While taking out insurance or funding retirement aren't the most exciting investments now, they could save you from financial challenges in the future.

7. Embrace your earning power.

If you're working entry-level jobs or getting by on sporadic freelance work, then it's hard to feel in control of your finances, warns Stefanie O'Connell, 29, author of "The Broke and Beautiful Life," a money guide for millennials, and contributor to the U.S. News Frugal Shopper blog. "Even if you reduce your monthly expenses to zero, you're only saving as much as you were once spending ... I tripled my income in 2015 and it's been absolutely life changing," she says.

O'Connell adds that given today's tough job market, millennials have to show initiative and aggressively pursue higher-earning opportunities. "Take the initiative to show how you contribute to the bottom line. It's hard to argue against a raise when you have the numbers and track record to back it up," she says.

8. Talk to your parents.

With parents still playing such an outsize role in so many millennials' financial lives, Jordan says parents and adult children should each make an effort to have open conversations about money. "Parents should take a proactive approach to shore up their own finances and teach children about responsible saving. Parents don't realize how much of a connection they're going to have; that conversation is really important, and they need to start early," Jordan says. On the flip side, millennials should also prepare to potentially assist their aging parents with money one day. "That's a conversation they really need to start having," he adds.

9. Keep things as simple as possible.

It's easy to feel overwhelmed with the various financial management choices you have, but the bottom line is that you need to save more and spend less to accumulate more wealth, says Erin Lowry, 26, founder of BrokeMillennial.com and contributor to the U.S News My Money blog. "Don't get so aggressive with paying down debt that you completely eliminate savings of any kind. Everyone should have at least $1,000 tucked away in an emergency savings fund," she adds. "The best way to shed the feeling of living on a tight budget is to cut spending while increasing your earning power."

That's exactly what she did: When she first moved to New York City in 2011, she was living paycheck to paycheck with a desirable but low-paying job in the entertainment industry. She picked up shifts at Starbucks, worked as a babysitter in her off-hours and severely limited her spending. Eventually, she created enough of a buffer that she could scale back her extra work (and catch up on sleep).

10. Always look for the next level.

Once you achieve a basic level of comfort with your savings and budgeting efforts, then it's time to tackle the next task. Perhaps it's fully filling your emergency savings fund, investing or opening a retirement account. "Don't get comfortable with your status quo," Lowry says. "Push yourself further by contributing another percent or 5 to your 401(k). Learn more about investing. Most importantly, set financial goals and make them specific."

For the past six years, Eliza Cross, a professional blogger and freelance writer in Denver, has put herself on what she calls a "money diet."

Not that she coined the phrase. "Money diet" is a term that's been around since at least the 1980s. For a stretch of time, maybe a week and often a month, you spend no money, except on essentials like groceries, gas and medicine. Unlike a food diet, where you want to lose pounds, the goal is to gain money. And if you do it right, Cross says, you should have more money than usual at the end of the month, and you may gain better financial habits as well.

Cross has been putting herself on a money diet every January, for all 31 days. She writes about it and commiserates with her readers on her blog, HappySimpleLiving.com.

And while Cross does it every January - "it's a good time of year when we're motivated to make changes in our lives, and a lot of us have been spending a lot over the holidays," she says - you can obviously go on a money diet any time. That said, some parts of the year are probably more challenging than others, such as the middle of summer, when you may want to do things like go on vacation, visit an old-fashioned ice cream parlor or take the kids to the water park.

It will help your cause if your family embraces the idea of a money diet. Cross is divorced and her oldest child is a grown-up, so that makes it easier for her than someone with an uninterested spouse and seven teenagers (although that hypothetical family would need the money diet more). Cross has a 13-year-old son, Michael, but so far, she says he has hardly noticed the extra-frugal periods.

Want to give it a try? Here's how to get yourself on a successful money diet.

Food means strictly groceries. You have to eat. But in the spirit of your money diet, you want to watch where you eat even more than what you eat.

"We don't pay extra for restaurant meals, takeout or pizza delivery," Cross says.

You'll also want to avoid buying a can of soda at the gas station. Try not to make eye contact when you pass kids selling candy bars for school. You also really shouldn't be going out for a cocktail with friends during a money diet, unless your pals are paying.

Visit your library. Before you yawn at what sounds like obvious advice, listen to Mike Catania, COO of the retail website PromotionCode.org. He is noticing a trend in which libraries allow you to check out things beyond books, CDs and DVDs.

For instance, Catania says, in California, "The Oakland Public Library lets you check out tools for DIY projects."

In fact, some libraries lend pretty unusual items. The Arlington Public Library, in Arlington County, Virginia, lends American Girl dolls out for a week. The Ann Arbor District Library in Michigan actually has a website titled, "Unusual stuff to borrow," and offers patrons the chance to check out things like telescopes and home-improvement tools like an indoor air-quality meter.

Even if your library doesn't offer anything unique to check out, you can get access to a lot of free entertainment.

Take on some part-time work. Or ask for extra hours. Or put in extra hours if you're on salary, assuming those hours will help you get ahead.

What's the rationale for working harder during your money diet? Well, you have less time to spend money.

Lamar Dawson, an account executive at a public relations firm in New York City, says he took on a part-time job on weekends in January 2014 to pay off student and credit card debt. First, he picked up cash by working in a Spider-Man costume for a toy store in Times Square, and then he became a host for an Italian restaurant, where he still works. And while he killed off his debt by December 2014, Dawson says the extra work inadvertently put him on a money diet.

"I found that it helped me save money because I wasn't at brunch with my friends, who were group texting me to come out for endless mimosas," he says.

Mystery shop. This is only practical if you plan, since mystery shopping gigs often take at least a few weeks to get set up. Nevertheless, what a great way to "cheat" and still completely be within your money diet.

Judy Williams, who works for an emergency fire and water restoration company in Saint Francis, Wisconsin, had what she and her husband called a "no-spend" month a couple of years ago.

During their money diet month, Williams was a mystery shopper, which is a part-time gig in which you're hired to go to stores or restaurants and pose as a customer (you make purchases, but the company hiring you reimburses you and often pays you a little extra).

"Not only did we get to eat out for free, I got paid to do so," Williams says.

Shop at home. Mystery shopping and working more is fine, but really, a money diet is more about notgoing out, since that can make you feel deprived if the temptation to spend is great. Instead, a money diet is a good way to get to know your home a little better.

You probably own a lot of things you never use, and this is a great time to start utilizing them, Cross says. "Use up the things we tend to hoard in our pantries, garages, medicine cabinets and closets," she says.

Did you discover that you have run out of soap or shampoo during your money diet? Those are essentials, and you can buy them without feeling guilty, but Cross points out that you might want to check first and see if you have some hotel soap or fancy shampoo that someone bought you a while back.

You can even grocery shop at home, Williams points out. During her money diet, she and her husband used many items they had stockpiled in the freezer.

Holly Wolf, based in Chester Springs, Pennsylvania, and the chief marketing officer at Conestoga Bank in Philadelphia, says she lives a frugal lifestyle and often does her grocery shopping at home.

"That mango barbecue that you had to have, figure out how to use it," she suggests. "Ditto for the pickled onions, the 10 pounds of ground chuck that was such a bargain, the frozen strawberries and the soup you froze a few months ago."

One of the side benefits of shopping in your own pantry or freezer, Wolf says, is that it should curb yourimpulse-buying the next time you're tempted to purchase something offbeat that you're not actually likely to eat.

And just as it's fun to window shop and find something you never would have dreamed of buying, you may end up making a similar "purchase" in your own home.

"One year, in my own house, I found a kit for insulating windows, and so I used that, and I wound up saving money on my energy bill," Cross says. "During a money diet, it's all about getting creative and using what you already have."

Looking for a business idea in a fast-growing sector? If so, you should steer clear of the industries below.

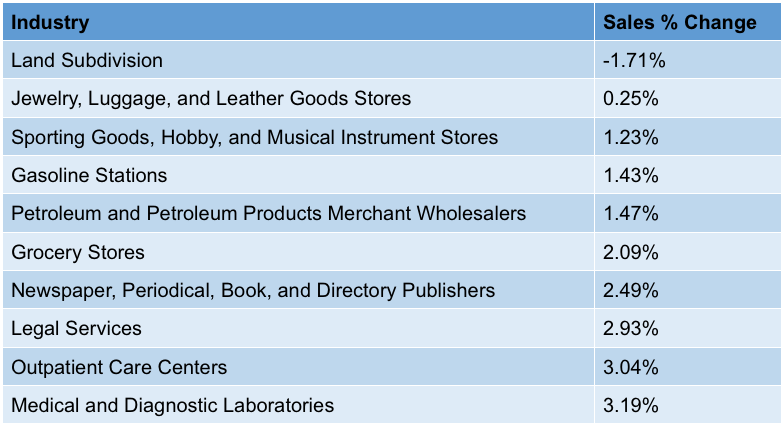

Sageworks has identified the industries that have experienced the slowest sales growth during the 12-month period ending October 23, 2015. At the top of the list is the Land Subdivision industry, comprised of companies dedicated to servicing land and subdividing real property into lots. Businesses in this sector have seen revenue contract 1.7 percent year over year. The bright side is, it's the only private company industry in the U.S. seeing negative revenue growth over the past year.

When an industry experiences contracting sales, a combination of internal and external factors are likely responsible, says Sageworks analyst Libby Bierman. Business owners witnessing a sales slowdown should take a close look at revenue models to determine problem areas, like underperforming locations or product lines.

In addition to land subdivision, retail is heavily represented on the slowest growing list. Retail industries included on this list were Jewelry and Luggage Stores, Sporting Goods and Musical Instrument Stores, Gasoline Stations, and Grocery Stores. Each of these four sub-sectors is growing revenues at an annual rate of less than 2 percent, compared to the average annual sales growth of 9.5 percent among all private companies.

One possible explanation for this slower rate of retail growth, of course, is the shift towards e-commerce and online retailers. Privately held brick-and-mortar retail companies are facing more competitive pressure than ever from online retail, as well as big box retailers.

"Even Amazon.com is becoming a common grocery store for some consumers," Bierman says.

The list also includes several industries within healthcare, such as Outpatient Care Centers and Medical and Diagnostic Laboratories. Inclusion on the list is far from a death sentence, however, as sales growth only tells part of the story, Bierman says. Without the context of other data, like net profit margin and previous periods' sales percent change, the most recent sales figures can be slightly misleading.

Legal Services is one industry where slow sales growth does not tell the full story, Bierman says. The growth may be slow but it is also consistent, and companies in this sector are much more profitable than the average private company.

Check out the table below for the full list of the slowest-growing sectors in the U.S.

Americans are increasingly whipping out plastic to pay for their purchases. This growing reliance on credit cards resulted in Americans closing out 2015 with more than $900 billion in credit card debt, according to a recent credit card study by CardHub.

That means the average U.S. household is shouldering the highest amount of credit card debt - more than $8,000 per indebted household - since the Great Recession.

It's a troubling (and disappointing) trend, especially when you consider just 18 months ago,many Americans reported either taking the scissors to their credit cards or making sure to pay off their balances in full each month. But more Americans seem to be practicing "swipe now, worry later" spending habits.

"Many consumers are focused on immediate gratification; it is very easy to pull out the plastic and make instant purchases," Laura Beal, a lecturer in finance, banking and real estate at the University of Nebraska at Omaha, told CardHub.

In addition to factors like income and financial literacy, CardHub said where you live plays a significant role in how well you manage your credit card debt and how high that debt rises.

According to CardHub, these 10 cities have the highest average credit card debt:

Beverly Hills, California: $13,583

Darien, Connecticut: $12,858

Westport, Connecticut: $12,220

Southlake, Texas: $11,512

Greenwich, Connecticut: $11,255

Highland Park, Illinois: $11,111

Colleyville, Texas: $11,107

Manhattan Beach, California: $10,721

Lake Forest, Illinois: $10,462

Calabasas, California: $10,444

These cities have the lowest average credit card debt:

Clarkston, Georgia: $2,705

Camden, New Jersey: $2,850

Coachella, California: $2,965

San Luis, Arizona: $3,028

Hamtramck, Michigan: $3,148

Delano, California: $3,150

Adelanto, California: $3,155

Laguna Woods, California: $3,300

Bell Gardens, California: $3,343

Lauderdale Lakes, Florida: $3,374

Here are some other interesting findings from CardHub's credit card debt study:

Based on residents' average credit card balance and income, College Station, Texas, has the longest estimated payoff timeline at 387 months (more than 32 years), which is 47 times longer than the shortest payoff timeline, 10 months, for Cupertino, California.

Americans added $21.3 billion in new credit card debt during the third quarter of 2015, which is 71 percent higher than the post-recession average.

Countless Americans ring in the new year determined to shed those few extra pounds around their midsection. But the new year is also a good time to sit down and take a good, hard look at your finances. Maybe you could add shedding debt to your list of New Year's resolutions?

If reducing your debt load seems overwhelming, just remember how great you would feel if you started 2017 with an extra $5,000 in your bank account.

First, take a look at your total debt. A recent NerdWallet study found that the average American household is shouldering $129,579 in debt - an alarming $15,355 of that on credit cards. That means the average American is forking over more than $6,600 each year in interest, roughly $2,600 of it for credit cards.

Yikes! But reducing the amount of money you're paying in credit card interest is sometimes just a phone call away, according to the New York Post,

"Few people ask a card company for a lower rate of interest," Matt Schulz, a senior analyst with CreditCards.com, told the Post. "However, if you have a pretty good payment record, we've found that most people who ask for it do get a lower rate."

Here are four more easy ways the Post says you can follow to get control of your finances and end 2016 with an extra $5,000 in savings:

Figure out where you're spending your money. Simply put, you need to compile a list of your expenses. "This sounds simple, but it's crucial: You need to know how much you make and what you spend it on. Then figure out what you can cut down on," Sean McQuay, a card analyst with NerdWallet, told the Post.

Spend less money. After you've compiled a list of your expenses, figure out where you can cut back so you can sock away some extra money in savings. For example, if you're spending $6 at Starbucks five days a week, you might want to start brewing your coffee at home instead. Cut back on eating out, pack a lunch and take it to work, and consider dropping your cable or downgrading to a cheaper cellphone plan. Check out "25 Ways to Spend Less on Food."

Make more money. "Freelance work, selling unused property or teaching classes online are some of the ways you can bring in some extra cash for paying down your debt," the Post explains. Paying down your debt means you're forking out less money for interest. (For more ideas, check out "20 Odd Ways to Make Extra Money.")

Create a realistic budget (and stick to it). Are there things you can reduce or eliminate from your budget? "Ask yourself: Do I really still need my cable subscription now that I'm on Netflix?" McQuay suggests. "Do I still need to have a landline phone? Do I still need that car I hardly drive? There are basic things consumers at any income level can do to increase their wealth." Check out "8 Secrets to Building a Budget You Can Live With."

According to the Post, those are four easy ways you can get a better grip on your finances and sock away up to $5,000 by 2017.

It's wintertime and that means it's time to hit the slopes. But as a lot of us know, planning a ski trip can quickly add up. Luckily, there are a few ways to enjoy that fresh powder without putting a dent in your savings.

First, renting skis at the lodge is costly and renting day of is even worse. So, if you don't already own skis, get them from a third-party rental house to save up to 30 percent off. If you have to rent from your lodge, try to reserve your skis online at least 48 hours in advance, and you should see discounts of up to 25 percent.

Next, try to buy your lift tickets online for more savings. At Liftopia.com, you can save an average of 27 percent off your lift tickets. Alternatively, you can check out larger ski and sporting retailers, such as Sports Authority and Dick's Sporting Goods. And don't overlook big box stores like BJ's, Sam's Club and Costco for some great deals.

Finally, look for all-inclusive ski packages to get the greatest value. Lift ticket and lodging packages are often great deals. Many hotels and B&Bs in ski towns negotiate special deals with resorts to offer ski tickets for free or discounted prices. Typically, you have to schedule these packages well ahead of time, so look into this option early to find the best deals.

Before you go on your next ski trip, remember these tips. You'll see that with a little pre-planning, going skiing doesn't have to be a slippery slope for your savings.

Winter is here, and that cold weather can affect your home and your savings. Luckily, there are a few things that can help you make it through the season and save a few bucks, too.